Hope and enthusiasm can only carry the market so high for so long

Waiting for the Fed’s Economic Forecast Update

What a week it’s been! We’ve received a solid February jobs report, endured a March snow storm and late last night even saw another round of would-be news on President Trump’s 2005 tax return. Those two later stories were far less newsworthy than was widely anticipated as Trump paid a 25 percent tax rate and winter storm Stella’s impact wasn’t as extreme as expected, although it did leave trading volumes rather light yesterday. They would have been so regardless, as the market is still in wait-and-see mode as it eyes today’s afternoon announcement from the Federal Reserve on interest rates.

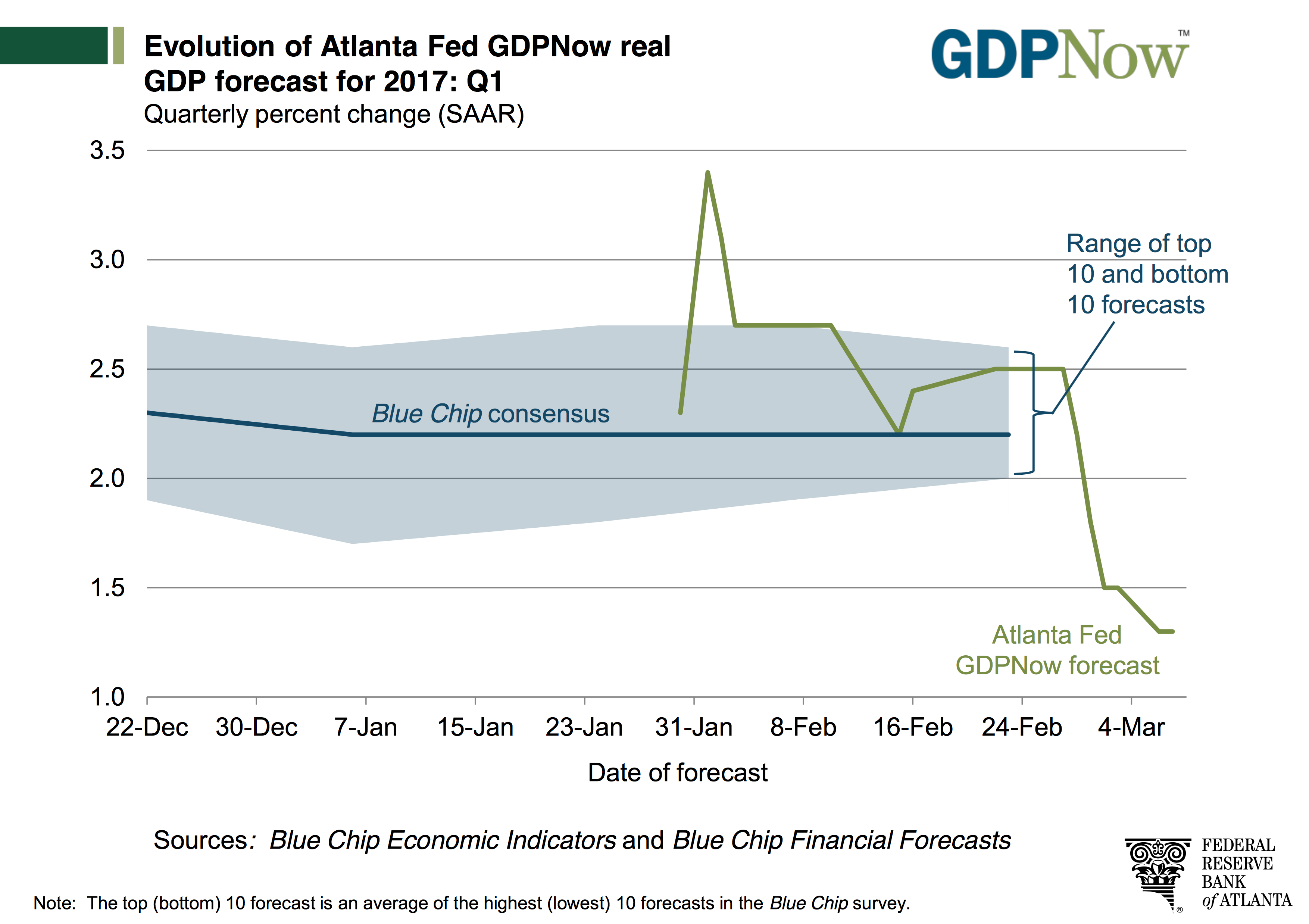

What was once thought of as a long shot, has reversed course and picked up steam with the market now widely anticipating the Fed to modestly boost interest rates. The rate increase is expected even though, as we pointed out in this week’s Monday Morning Kickoff, the Atlanta Fed has done nothing but trim its GDP expectations for 1Q 2017 over the last few weeks. Odds are, today’s latest iteration of that GDPNow report will see a boost up from the dismal 1.2 percent reading owing to the February Employment Report, but it will be hard pressed to break past the 1.9 percent GDP print for 4Q 2016.

Keeping in mind the Fed has a knack for boosting interest rates at the wrong time, and it looks increasingly like Trump’s fiscal policies will take longer than many have expected to take hold and boost the economy, we here at Tematica will continue to tread prudently and cautiously in the near-term.

Hope and enthusiasm can only carry the market so high for so long.

Yes, each week we continue to see confirming data points for our 17 investment themes, which you can see in our Friday missive that is Thematic Signals, but we remain concerned over the market’s stretched valuation and the simple fact that expectations have to catch up with the current economic reality.

Now when many hear talk like that, the first reaction is to get nervous. It’s understandable, but we’re not suggesting a market correction is coming. Even though there are signs the economy has slowed, it is still growing as evidenced by the recent reports from Markit Economics and ISM. Our thinking is that a market pullback — something we define to be in the 3-6 percent range — may not be popular to all the recently returned investors, but it would take, to quote former Fed Chief Alan Greenspan, some of the “irrational exuberance” out of the market. Not a bad thing as it would allow us to revisit some thematic contenders that have moved higher and faster than they probably should over the last four and a half months.

Like Warren Buffett is often quoted saying, “Price is what you pay, value is what you get.”

We couldn’t agree more.

Aside from the now largely expected interest rate increase itself, let’s remember the Fed tends to be very vague in its language and the market has a habit of not really listening to what the Fed is trying to communicate. As the Fed boosts interest rates, we’re likely to get an update on its economic and inflation forecasts in its policy statements and its that language that will either soothe the market or give it some indigestion.

You’ve probably come to the conclusion that it’s best to stand pat for now, and we certainly agree.

We’ve got a number of positions on the Tematica Select List that are benefitting from pronounced multi-year tailwinds, like Connected Society company Dycom Industries (DY) and the 5G deployment; Disruptive Technology plays Universal Display (OLED) and Applied Materials (AMAT); Aging of the Population and AMN Healthcare (AMN) and the PureFunds ISE Cyber Security ETF (HACK) that is part of our Safety & Security investing theme to name just a few.

Two stocks we will be watching closely are Food with Integrity United Natural Foods (UNFI), which reported good quarterly earnings last week and recently stopped out Costco Wholesale (COST) shares. Both stocks drifted lower last week, with UNFI a tad below the average cost basis of $42.95 on the Tematica Select List and Costco shares breaking through their 50-day moving average at $167.34. When we’ve seen such moves in COST shares previously, it tends to take more than a few weeks for the shares to settle out. Given our Cash-strapped Consumer investing theme and the Costco’s continued expansion, as well as announced membership price hike, that should drive membership-related profits higher.

- We’ll continue to keep our eyes on COST for an opportunity to jump back in.

Ways to Get Prepared for Future Moves

Be sure to listen to the latest edition of Cocktail Investing, in which Tematica Chief Macro Strategist Lenore Hawkins and I talk with Steve Fredette of Toast, a restaurant technology company at the intersection of the Connected Societyand Asset-lite investment themes. We’ll have another episode out tomorrow that will wrap up all the key market and economic data with a special guest Jack Mohr, who up until recently worked with Jim Cramer — yes that Jim Cramer — managing his Action Alerts Portfolio.

Be sure to listen to the latest edition of Cocktail Investing, in which Tematica Chief Macro Strategist Lenore Hawkins and I talk with Steve Fredette of Toast, a restaurant technology company at the intersection of the Connected Societyand Asset-lite investment themes. We’ll have another episode out tomorrow that will wrap up all the key market and economic data with a special guest Jack Mohr, who up until recently worked with Jim Cramer — yes that Jim Cramer — managing his Action Alerts Portfolio.

Also be sure to come back to Tematica Investing during the week to see our latest thoughts and comments on the economy, the market and stocks, both in and out of the Tematica Select List.