Weekly Issue: Adding Two Calls Ahead of the Holiday Season

Key points in this issue

- We are issuing a Buy on and adding the Amazon (AMZN) Feb 2019 2000.00 (AMZN190215C02000000) calls that closed last night at 146.30 with a stop loss at 100.00.

- We are issuing a Buy on and adding the United Parcel Service (UPS) January 2019 120.00(UPS190118C00120000) calls that closed last night at 3.58 with a 2.50 stop loss to the Select List.

- With a number of headwinds staring down the market as we head into 3Q 2018 earnings season, we will continue to hold the ProShares Short S&P500 (SH) November 2018 28.00 (SH181116C00028000) calls that closed last night at $0.22. With that position little changed since we added it last week, our 0.14 stop loss remains intact.

- We will continue to hold the Universal Display (OLED) January 2019 130.00 calls (OLED190118C00130000) that closed last night at 11.05, up just over 25% since their addition two weeks ago. Given the move, we will increase our stop loss to 7.00 from 4.00.

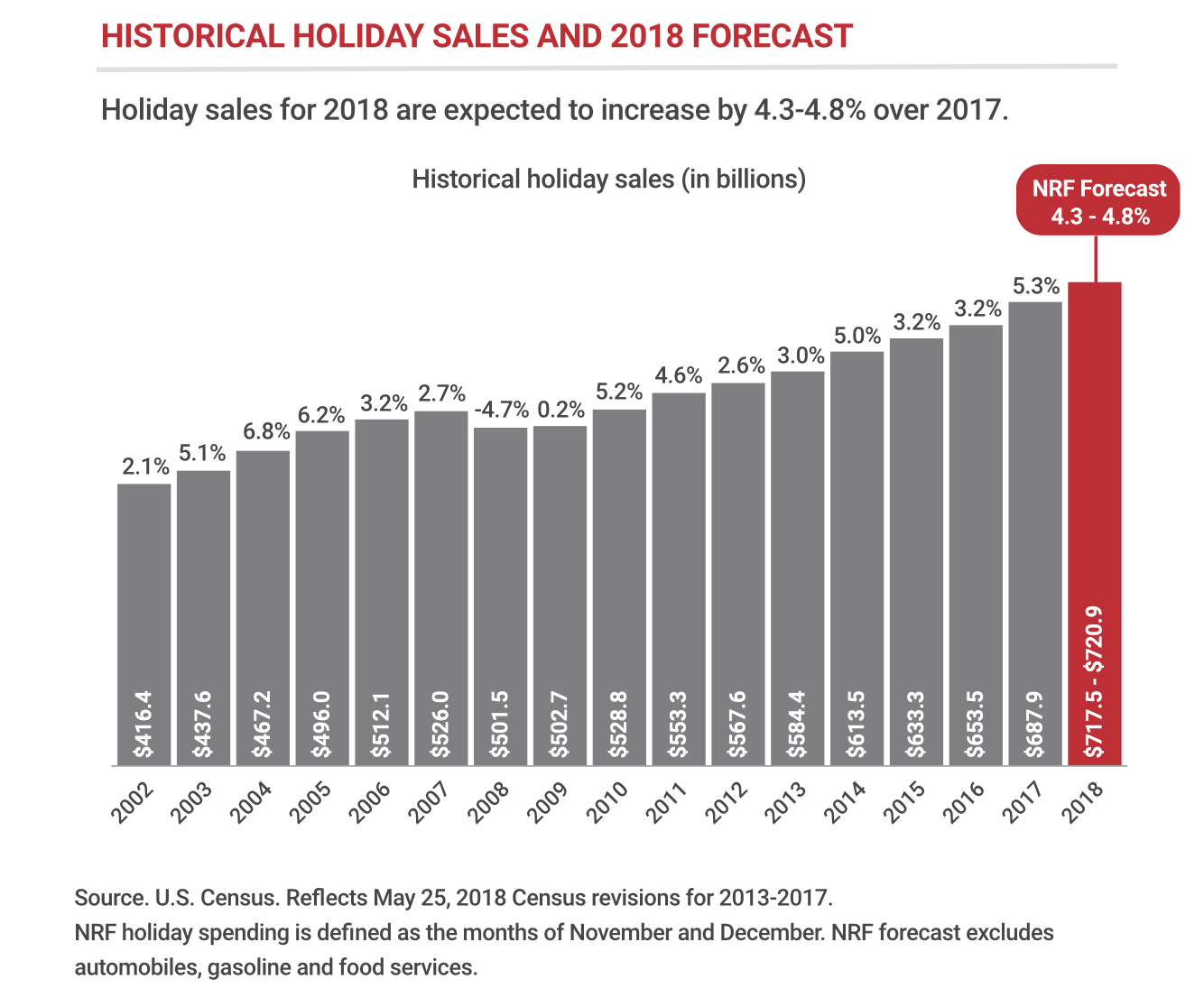

The NRF issues its 2018 holiday spend forecast,

and we add 2 new call positions

Yesterday, the National Retail Federation published its 2018 holiday retail sales forecast, which covers the November and December time frame and excludes automobiles, gasoline, and restaurants sales. On that basis, the NRF expects an increase between 4.3%-$4.8% over 2017 for a total of $717.45- $720.89 billion. I’d note that while the NRF tried to put a sunny outlook on that forecast by saying it compares to “an average annual increase of 3.9% over the past five years” what it did not say is its 2018 forecast calls for slower growth compared to last year’s holiday shopping increase of 5.3%.

That could be some conservatism on their part or it could reflect their concerns over gas prices and other aspects of inflation as well as higher interest costs vs. a year ago that could sap consumer buying power this holiday season. Last October the NRF expected 2017 holiday sales to grow 3.6%-4.0% year over year, well short of the 5.3% gain that was recorded so it is possible they are once again underestimating the extent to which consumers will open their wallets this holiday season. While I am bullish, we can’t rule out there are consumer-facing headwinds on the rise, and that is likely to accelerate the shift to digital shopping this holiday season, especially as more retailers prime the digital sales pump.

On its own Amazon would be a natural beneficiary of the seasonal pick up in shopping, but as I’ve shared before it has been not so quietly growing its private label businesses and staking out its place in the fashion and apparel industry. These moves as well as Amazon’s ability to competitively price product, plus the myriad way it makes money off its listed products and the companies behind them, mean we are entering into what should be a very profitable time of year for Amazon and its shareholders.

We already own the shares in Tematica Investing, but for some extra oomph here at Options+ I’m adding the Amazon (AMZN) Feb 2019 2000.00 (AMZN190215C02000000) calls that closed last night at 146.30. That strike price will capture the company’s December 2018 quarter earnings report as well as the post-holiday shopping that tends to happen each and every year.

As we move through the soon to be upon us September quarter earnings season, I’ll be assessing and collecting other retail outlooks for this holiday shopping season. Given the timing for this option position, I’m going to set a wider than usual stop loss at 100.00, and as the calls move higher, I’ll look to tighten it up.

- We are issuing a Buy on and adding the Amazon (AMZN) Feb 2019 2000.00 (AMZN190215C02000000) calls that closed last night at 146.30 with a stop loss at 100.00.

I’ve long said that United Parcel Service (UPS) shares are a natural beneficiary of the shift to digital shopping. With a seasonal pickup once again expected that has more companies offering digital shopping and more consumers shopping that way, odds are package volumes will once again outpace overall holiday shopping growth year over year. From a financial perspective, that means a disproportionate share of revenue and earnings are to be had at UPS, and from an investor’s perspective, that means multiple expansion is likely to be had. Therefore, as we add those Amazon calls to our holdings, we will also do the same with UPS as follows:

- We are issuing a Buy on and adding the United Parcel Service (UPS) January 2019 120.00(UPS190118C00120000)calls that closed last night at 3.58 with a 2.50 stop loss to the Select List.

As warnings flares are had, we’re sticking with our S&P 500 inverse calls

This week we received some favorable September economic news in the form of the ADP Employment Report as well as the ISM Services Index with both crushing expectations. Despite these reports, has barely budged this week, which suggests to me investors are expecting a sloppy September quarter earnings season for the market. No doubt there will be some bright spots, but in aggregate we are seeing a number of headwinds compared to this time last year that could weigh on corporate outlooks.

Already we’ve had a number of companies issuing softer than expected outlooks due to rising input costs, trade and tariffs, the slower speed of the economy compared to the June quarter, and concerns over higher gas prices and the impact on consumers. A great example of that was had yesterday when shares of lighting and building management company Acuity Brands (AYI) fell more than 13% after it reported fiscal fourth-quarter profit that beat expectations, but margins fell amid a sharp rise in input costs. The company said costs were “well higher” for items such as electronic components, freight, wages, and certain commodity-related items, such as steel, due to “several economic factors, including previously announced and enacted tariffs and wage inflation due to the tight labor market…”

Acuity is not the first company to report this and odds are it will not be the last one as September quarter earnings begins to heat up next week. As the velocity of reports picks up, we could be in for a bumpy ride as investors reset their growth and profit expectations for the December quarter and 2019. Therefore, we will continue to hold over inverse S&P 500 calls, which thus far are little changed from where we added them last week.

- With a number of headwinds staring down the market as we head into 3Q 2018 earnings season, we will continue to hold the ProShares Short S&P500 (SH) November 2018 28.00 (SH181116C00028000)calls that closed last night at 0.22. With that position little changed since we added it last week, our 0.14 stop loss remains intact.

Checking in on our Universal Display calls

Over the last few weeks, we’ve seen a growing reception for Apple’s (AAPL) new iPhone models, both of which utilize the organic light emitting diode display technology that is made possible by Universal Display’s chemical and intellectual property business. We’ve also started to see adoption outside of Apple with other smartphone companies and in other markets as well (TVs, automotive lighting), which confirms to me adoption rates are on the upswing. This bodes very well for Universal’s business in the second half of 2018 and beyond as well as our January 2019 calls.

The next known catalyst for OLED shares and these calls is November 1, when Apple will report its September quarter results. I’ll be on the lookout for additional signs of OLED adoption between now and then, but for now let’s stick with our OLED calls.

- We will continue to hold the Universal Display (OLED) January 2019 130.00 calls (OLED190118C00130000)that closed last night at 11.05, up just over 25% since their addition two weeks ago. Given the move, we will increase our stop loss to 7.00 from 4.00