With Obamacare Here to Stay, Investors Re-Think Growth

DOWNLOAD THIS WEEK’S ISSUE

The full content of The Monday Morning Kickoff is below; however downloading the full issue provides detailed performance tables and charts. Click here to download.

Welcome back to another issue of the Monday Morning Kickoff. Last week we shared our view that the stock market is coming to grips with something we’ve been talking about quite a bit over the last several weeks: the growing disconnect between the speed of the domestic economy, earnings expectations and the steady rise in the stock market through the end of February. We dug deep into this during last week’s Cocktail Investing Podcast, which if you missed it — and shame on you for doing so — you can find it here. Also, last week Tematica’s Chief Macro Strategist had a great write up detailing the “how’s” and “why’s” it’s truly different this time around for all of those folks comparing the Trump opportunity with the economic boom we saw under President Reagan. In our view, it’s a must-read and you can find that here. Finally for those of you that have asked for a more comprehensive way to utilize in our various investment themes, hang on just a wee bit longer as we’ve got some pretty cool stuff coming your way in 2Q 2017.

Passengers, please fasten your seatbelts

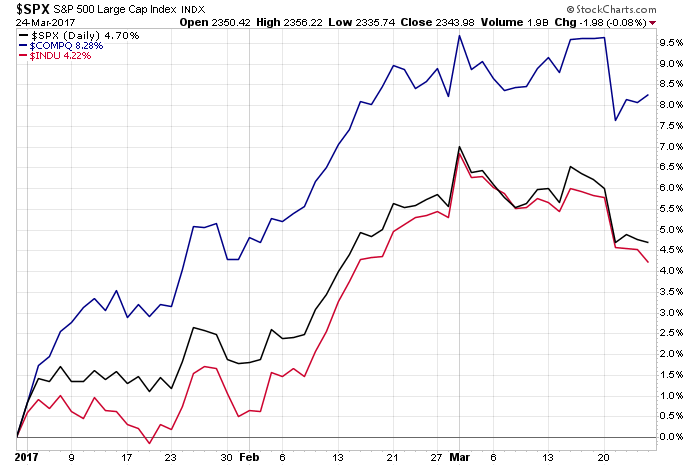

All of the major indices fell more than 1.2 percent last week, with the Dow Jones Industrial Average falling the most at 1.5 percent. After several months of a smooth and steady climb, it felt much like hitting a patch of turbulence while on a cross-country flight.

There were several reasons for the move lower, which in our view can be summed up with the simple fact that investors are focusing more and more on the growing disconnect that has been emerging in the markets, with the speed of the domestic economy not in sync with earnings expectations and the price of the markets through the end of February. Adding fuel to the fire is the stalled momentum in Washington as the new administration has had a number of snafus to deal with that has pushed the back timing for more economically stimulative policies like infrastructure spending and tax reform. The pulling of the GOP health plan before the vote last Friday afternoon was another blow, which means the Affordable Care Act is here to stay (at least for the foreseeable future), and it also means the Trump administration will turn its focus to other matters.

Candidly, we would have preferred Team Trump work on infrastructure spending and tax reform first, which we think would have led to more political capital and eased an overhaul of the ACA later. But, campaign promises are campaign promises and here we are. It likely means that much as we’ve been saying, we won’t see any meaningful policy-led pick up in economic activity until 2018. Odds are the stock price pressure we saw last week in healthcare and related stocks that fall under our Aging of the Population investing theme will see some relief lift this week. From our vantage point, despite our Fountain of Youth investing theme, there is no reversing the aging process, at least not yet, and given our current demography, there is much spending coming in and on healthcare.

Getting back to the topic at hand, all of this is leading investors to rethink growth expectations, and we’re seeing that reflected in 1Q 2017 earnings expectations. As we’ve mentioned previously, over the last several weeks the Atlanta Fed has been moving its GDPNow forecast for the current quarter lower. It started off at more than 3 percent in January and fell to a low last week of 0.9% before being revised modestly higher to a whopping 1.0 percent on Friday.

Then we received the March Flash US Composite PMI, which showed manufacturing and services tumbled to multi-month lows with businesses once again becoming cautious per the move lower in new order activity. We also saw another tick up in input cost inflation per Markit’s findings with “the overall rate of input price inflation was the fastest for two-and-a-half years. Efforts to pass on higher costs contributed to an upturn in factory gate price inflation to its strongest since November 2014.”

In our view, all of this is more evidence of looming stagflation. Also on Friday, we received the February Durable Orders report, which on its face was better than expected, but stripping out aircraft and defense-related items core capital goods fell 0.1 percent month over month. Paired with a 0.1 percent increase in January, this report is not exactly a harbinger of strong business investment.

In short, all of these are reasons to think the current quarter’s GDP is apt to be much slower than 4Q 2106’s 1.9 percent reading.

Now let’s turn from the speed of the economy to earnings expectations…

As we entered 2017, the expectation was the 500 S&P companies would grow their collective earnings more than 12 percent, compared to 2016. Even before we get March quarter results, the view on 2017 earnings growth for the S&P 500 has fallen to just over 10 percent.

As we’ve noted in recent editions of the Monday Morning Kickoff, earnings expectations for March quarter have started to move lower in recent weeks, but even so, the estimated earnings growth rate for the S&P 500 is 9.1 percent. If that 9.1 percent is the actual earnings growth rate for the quarter, it will mark the highest year-over-year earnings growth reported by the index since Q4 2011’s 11.6 percent. Given the data we’ve been seeing, we would have to say there is more downside risk to be had than upside surprise for that forecast. With several highly anticipated Trump policies getting pushed out and more economic data pointing to a once again slowing economy, odds are companies will have to reset EPS expectations for 2Q 2017 and most likely 3Q 2017 as well, which means we are likely to see full year 2017 expectations come down further.

As this happens, the market will likely continue to wake up to current valuation levels, especially since if the price of the S&P 500 remains steady and earnings get cut, the market valuation will climb. Odds of that happening are rather low given the market’s stretched valuation and it would mean paying more for even slower earnings growth. Taken all together, we’re likely to see the market move lower over the coming weeks as all of these expectations get rejiggered lower.

After Friday’s market close there are just five trading days left in the quarter and a number of companies have already entered their “quiet periods.” This means we’re going to have our scopes up for potential earnings pre-announcements. If we get more than usual, or from some larger blue-chip and tech companies, we could see the market get a little bouncy compared to the last few months.

In times like this, using our thematics as a guide and checking recent data points, we’ll look to scale into positions on the Tematica Select List and contemplate adding new ones where it makes sense.

What’s On Tap for The Week Ahead

Looking at the last five trading days of the month a little more closely, we’ll get the third estimate for 4Q 2016 GDP as well as February Personal Income & Spending. Candidly, we’re not expecting much on the lasted 4Q 2016 GDP revision, but rather what it may mean for the current quarter should it get revised modestly higher. With roughly two-thirds of the economy tied directly or indirectly to consumer spending, the February Personal Income & Spending report could lead economist to tweak their GDP models one way or the other. Given several reports from Wells Fargo (WFC) and investment firm Cowen that paint an even weaker retail environment than they had been expecting, odds are likely the personal spending component of that report could come up a tad short.

As we mentioned above, the majority of companies will be heading into their respective quiet periods ahead of March quarter results and that means a dramatic slowdown in investment conferences. There is one major one on the docket — the Sidoti and Company Spring Emerging Growth Convention 2017, which will have a variety of smaller cap companies on tap and ETF investors should be mindful of the iShares S&P SmallCap 600 Index ETF (IJR) and the iShares S&P SmallCap 600 Growth ETF (IJT) as that conference gets underway.

Even though there is a dramatic slowdown in earnings reports to be had, there are several that we’ll be dialing into to get the latest as it relates to our Affordable Luxury, Fattening of the Population and Rise & Fall of the Middle Class investing themes. That means examining reports from Darden Restaurants (DRI), Sonic (SONC), Dave & Busters (PLAY) and Restoration Hardware (RH) as well as Lululemon (LULU) and McCormick & Co. (MKC) this week. The results, commentary and guidance from these companies should not only give us a gauge on the consumer mindset and spending, but also shifting consumer preferences that would power McCormick & Co. at the expense of Darden and Sonic for example. Thematic tailwinds and headwinds in other words. As usual, there is a more detailed list of earnings reports coming this week from a thematic perspective below.

Enjoy the week ahead and we’ll see you back here next week. In between, be sure to check our Tematica Research for more of our thoughts and insights during the week, and be sure to catch the next episode of Cocktail Investing.

Thematic Earnings Calendar

The following are just some of the earnings announcements we’ll have our eye on for thematic confirmation data points:

Affordable Luxury

- Restoration Hardware (RH)

Asset-lite Business Models

- FTI Consulting (FCN)

- IHS Markit (INFO)

- Verint Systems (VRNT)

Cash-strapped Consumer

- Ollie’s Bargain Outlet (OLLI)

Connected Society

- Blackberry (BBRY)

Economic Acceleration/Deceleration

- Worthington Industries (WOR)

Fattening of the Population

- Darden Restaurants (DRI)

- Sonic Corp. (SONC)

Guilty Pleasure

- Dave & Busters

Rise & Fall of the Middle Class

- Bassett Furniture (BSET)

- Cal-Maine Foods (CALM)

- Carnival (CCL)

- G-III Apparel (GIII)

- Lululemon Athletica (LULU)

- McCormick & Co. (MKC)