Something Just Isn’t Adding Up in the Recent Data

The week started off strong out of the gate on Monday in the wake of Friday’s post-payroll rally, but the momentum quickly faded, leaving the S&P 500 down four consecutive days as of Thursday’s close. If it closes in the red again Friday, it will be the longest losing streak in over 16 months going back October 31st, 2016. We dug into the details of the recent data and in this week’s edition, we point out some things that just aren’t jiving.

Wednesday the Industrials sector fell below its 50-day moving average with Boeing (BA) leading the decline as the weakest performer in the Dow, also falling below its 50-day moving average. In the Materials sector Century Aluminum (CENX) fell below its 50-day moving average to lead metals lower. DowDupont (DWDP) also failed to rise above its 50-day moving average. Thursday the Dow Transports sector followed Industrials, falling below its 50-day moving average and finding resistance at its late February peak.

The strongest performing S&P 500 sector over the past five days has been Utilities, followed by Real Estate – not exactly typical bull market leaders. After having experienced one of the strongest starts to a year, the S&P 500 is up less than 3% from December’s close and ended Thursday below its 50-day moving average. Technology has been the only sector to reach a new record high, but its technical indicators are starting to weaken, so this one looks to be over-extended. By Thursday’s open the percent of stocks in the S&P 500 trading above their 50-day moving average was down to 43% with over 22% of stocks in oversold territory and 21% in overbought.

Bonds

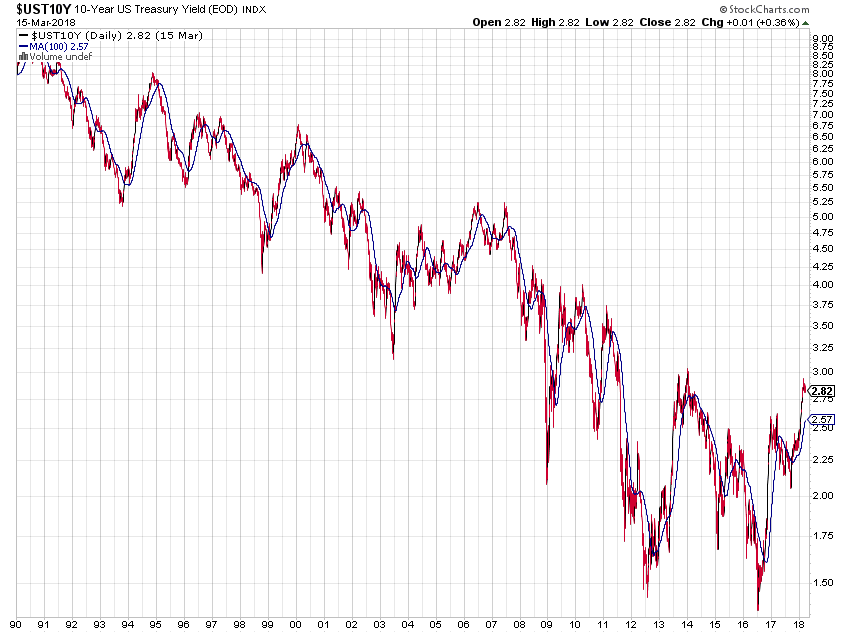

US 10-year Treasury yield broke above its 100-month moving average in November of last year for the first time since July 2007 and hasn’t looked back. That being said, while the yield for the 10-year recently peaked on February 21st at just shy of 3% and has fallen roughly 12 basis points since then, the S&P 500 hasn’t been able to make much progress.

Meanwhile, no one seems to be talking about how we are seeing flattening in the yield curve.

The Consumer

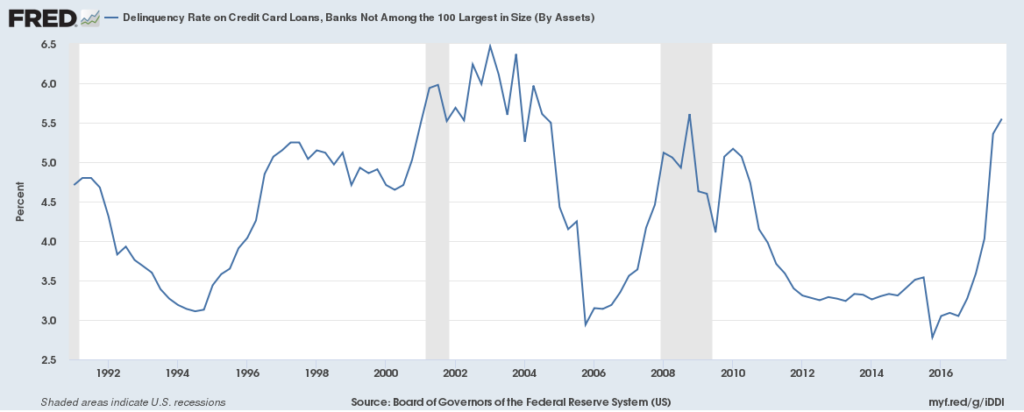

February Retail Sales were weaker than expected, declining for the third consecutive month, the longest such streak in three years. Then again, the month-over-month change in average hourly earnings for all employees has been either flat or negative in 6 of the past 7 months and in the fourth quarter of 2017, consumers racked up credit card debt at the fastest pace in 30 years – bad for consumer spending, but rather confirming for our Cash-strapped Consumer investing theme. Most concerning is that credit card delinquencies at smaller banks have reach levels not seen since the depths of the Great Recession.

Corporate America

Homebuilder sentiment, after reaching the highest level since 1999 this past December, has now declined for 3 consecutive months, but even so, it still remains at nearly the highest levels since the financial crisis. Meanwhile, the NAHB Housing Market Index has fallen 17% from the January 22nd high and its most recent report found a significant downturn in traffic, perhaps due to rising mortgage rates as the 30-year fixed rate has reached the highest level in over 4 years. Perhaps the weakness has something to do with the aforementioned lack of wage growth as the ratio of the average new home price to per capita income has again reached the prior peak of 7.5x – people just can’t afford it.

We’ve been warning of the dangers of exuberant expectations for a while here at Tematica. The General Business Conditions Average for manufacturing from the Philadelphia & New York Fed this week illustrated just why we have. The two saw a small uptick in March after having been weakening in recent months. However, the outlook portion, which had been looking better in the past is now showing some weakness. For example, CapEx expectations 6-months out fell in March from the highest levels on record in February. Expectations around Shipments also dropped, having been at the second-highest levels of the current expansion. After having reached extreme levels in November, New Order expectations also declined. When sentiment expectations reach new highs, tough to continue to rise significantly from there.

While Friday’s job report got the markets all excited, perhaps the reason that enthusiasm has cooled is folks are realizing that the 50k gain in retail jobs isn’t syncing up with the -4.4% SAAR decline in retail sales over the past three months. Then there is what we are hearing from the horses’ mouth. Walmart (WMT) and Target (TGT) both issued weak guidance, as did Kroger (KR) who also suffered from shrinking margins. A tight and tightening job market is unlikely to help with that. Costco (COST) missed on EPS, as did Dollar Tree Stores (DLTR), who also missed on EPS and gave weaker guidance. Big Lots (BIG) saw a decline in same-store sales. At the other end of the spectrum, the 70k gain in construction is in conflict with rising mortgage rates, traffic and declining pending home sales, while the 31k gain in manufacturing has to face a dollar that is no longer declining, high costs on tariff-related goods and potentially some sort of trade war.

Inflation

As I mentioned above, while real retail sales fell -4.4% SAAR over the past three months, Core Consumer Prices rose 3.1% SAAR and Wednesday’s Producer Price Index (PPI) report from the Bureau of Labor Statistics also showed rising inflation pressures. Core PPI (yoy) has reached its highest levels since 2011 with the annualized 3-month trend having gone from 1.5% last summer, to 2.7% at the end of 2017 to 3.4% based on the latest data.

Import prices for February rose 0.4%, taking the year-over-year trend up to 3.5% from 3.4%. Recall that last summer this was around 1%. Ex-fuel the pace rose to 2.1% from 1.8% previously and 0.8% over the summer.

The bottom line this week is that we are no longer in the easy peasy 2017 world of hyper-low volatility and relentlessly rising indices with a VIX that has found a new normal more than 50% above last year’s average. The wind up is the major market indices haven’t been able to commit to a sustained direction. The hope and promises of 2017 have been priced in, leaving us with a, “So now what?” which is reflected in the Atlanta Fed’s GDPNow forecast falling from 5.4% on February 1st to a measly 1.8% on March 16th – talk about a serious fade.

What has us really concerned is that at a time when big job gains are making all the headlines we see credit card delinquencies at the level last seen in the depths of the Financial Crisis and retail sales contracting at a 4.4% annual rate over the past three months. This is the best we can get with a booming job market? Something here just isn’t right.

This is the best we can get with a booming job market? Something here just isn’t right.