Weekly Wrap: Where Do We Go From Here?

A Look Back at the Week of July 30 to August 3, 2018

Markets

Monday was a rough one with only three sectors closing in positive territory – financials, healthcare and energy. Technology continued to be the weakest sector, thanks to Facebook’s (F) faceplant followed by Twitter’s (TWTR) flail, which left analysts scrambling to rethink their earnings estimates.

Tuesday, the last day of July, was a cheerier one for those sweating it out on Wall Street — holy cow what a summer we are having this year from Dublin to Dubai, Stockholm to Sacramento. The Russell 2000, which had been pretty weak throughout July doubled the performance of the other major indices for the day. For the month the S&P 500 gained 3.3%, the Russell 2000 1.0%, the Nasdaq 1.4%, the Russell 1000 3.0% and the Dow Jones Industrial Average finished with the gold, up 4.6%. Year-to-date the indices were 5.8%, 8.7%, 12.0%, 5.2% and 2.5% respectively at the end of July.

Wednesday was all about Apple (AAPL), which delivered solid results in the June quarter and raised guidance. While energy was a star on Monday, it fell over 1% Wednesday, finishing in the red alongside Industrials and Materials as markets reacted to the news that the Trump administration may impose 25% tariffs instead of the earlier proposed 10% tariffs on $200 billion of Chinese imports. These tariff threats are starting to feel like a geopolitical version of whack-a-mole.

Thursday the Nasdaq and S&P 500 benefited from Apple’s rally of +2.9% to close the day as the first company ever to reach a $1 trillion market cap, $1.004 trillion to be more precise. The Nasdaq and the S&P rose +1.3% and +0.5% respectively while the Dow Jones Industrial Average closed roughly flat.

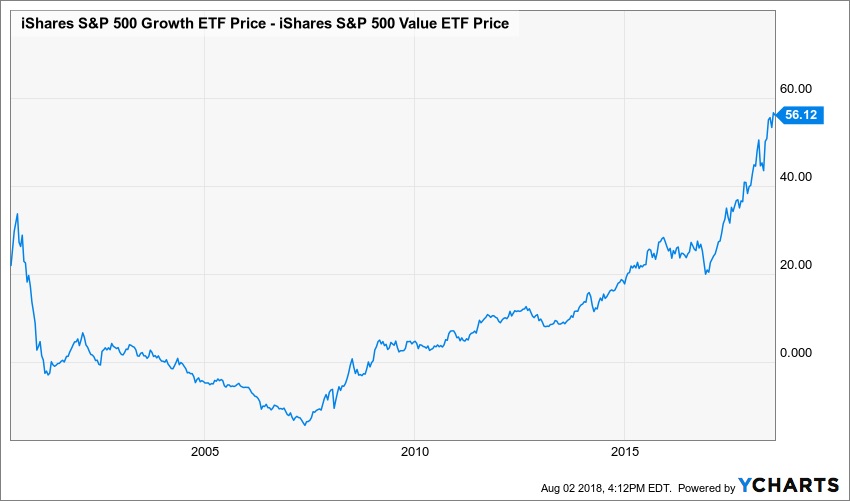

As we head into what is the seasonally most vulnerable part of the year for the markets we may be seeing a change in leadership. Since mid-2007, we’ve seen growth outperform value, as is illustrated in the chart below which shows the relative performance of the iShares S&P 500 Growth ETF (IVW) versus the iShares S&P 500 Value ETF (IVE).

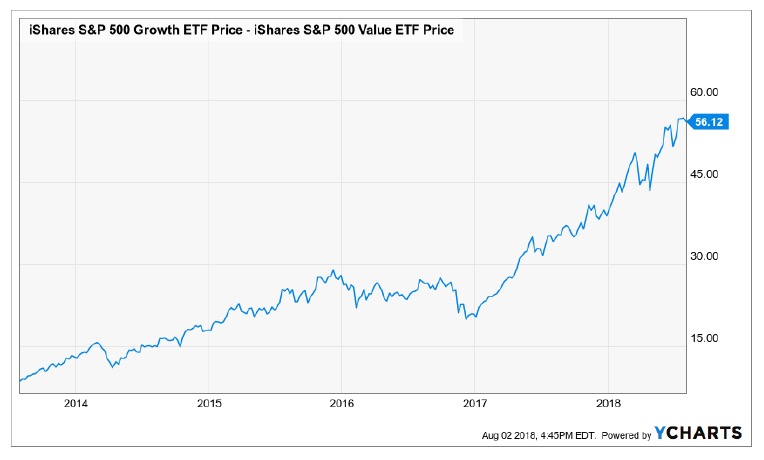

When the line is trending down, Value is outperforming Growth. When trending up, Growth is outperforming Value. Growth has been absolutely trouncing Value since June 2007, with the exception of October 2016 – January 2017 when Value took the lead, albeit briefly. This trend accelerated significantly in 2017, as the chart below shows.

When the line is trending down, Value is outperforming Growth. When trending up, Growth is outperforming Value. Growth has been absolutely trouncing Value since June 2007, with the exception of October 2016 – January 2017 when Value took the lead, albeit briefly. This trend accelerated significantly in 2017, as the chart below shows.

In 2018 the performance of the S&P 500 was driven primarily by the FAANG stocks – Facebook, Apple, Amazon (AMZN), Netflix (NFLX), Google (Alphabet – GOOG) – plus Microsoft (MSFT). At the end of June, when the market had fallen 5% below the January 26th high for 2018, those six stocks had contributed more than 100% of the then year-to-date gains – seriously narrow market leadership. Today they represent just over two-thirds as many of the more value-oriented stocks have shifted from a drag to a contributor. Further analysis (hat tip to Bespoke Investment Group) finds that the 50 stocks in the S&P 500 that had the highest returns in 2018 through July 25th have lost nearly 4% since then. Conversely, the 50 worst performers have declined over 1.5%. The best are now the worst and vice versa. This flip-flop in which performance through late July is inverted continues across the deciles of the S&P 500. This is by no means a trend yet, but worth watching.

This earnings season has also seen those that performed at or only slightly better than expected often getting their shares hit. Take a bow Caterpillar (CAT). This combo of strong earnings that haven’t been rewarded as well as in previous quarters has seen the S&P 500 trailing P/E ratio drop to the mid-20s from a post-recession high of 23.4 at the end of January – the largest such decline in trailing P/E in this cycle. Please excuse a slight pat on the back here as we’ve been warning that shares have been priced to ultra-perfection here, so just meeting expectations has been a disappointment in many cases.

The Economy

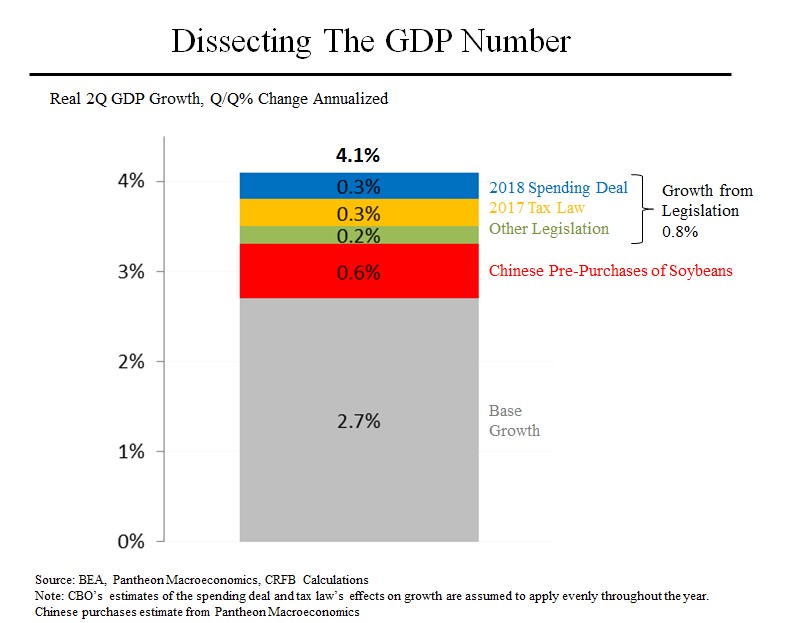

While we certainly love to see the economy doing well – it makes our jobs easier – last week’s Q2 GDP report had a decent share of factors that will not continue in the coming quarters, as we discussed here last week. Pantheon Macroeconomics did some great work breaking it down further. Excluding additional 2018 federal spending package, the 2017 tax reform, a few other minor legislative changes and the pull-forward in demand from China for soybeans, GDP would have been roughly just 2.7%.

The repeatable part of Q2 just wasn’t that spectacular and we are concerned that we see signs of slowing in the back-half of 2018.

Tariffs have become more and more of a topic, with references to tariff concerns all over the comments from respondents in the ISM Manufacturing report for July. On top of that, the word “tariff” was mentioned 290 times in S&P 500 conference calls in the first quarter. So far this quarter that number is up to 609, and we are just halfway through.

On the plus side:

- Personal Consumption ended the second quarter at the fastest real pace since 2014 – that tax break finally kicked in and folks spent!

- ISM Manufacturing report for July was weaker than expected, but still at a strong level, dropping to 58.1 from 60.2 versus expectations for a decline to 59.4. To put those numbers into context, anything over 50 is expanding and the index is today less than three points away from its February multi-year high of 60.8.

- Home prices increased faster than expected in May, rising 6.5% versus the anticipated 6.4% with some markets starting to look overheated.

- The Fed sounded impressed as the statement this week following their policy meeting saw a slight shift in tone from what was “…economic activity has been rising at a solid rate” to “…economic activity has been rising at a strong” (Emphasis mine). Overall the word “strong” appeared six times in this month’s statement versus four in the prior.

- Unemployment claims for the week ending July 29th were less than the 220k coming in at only 180k. This comes after claims dropped to 208k the week ending July 14th, the lowest level since December 1969.

- ADP’s private sector employment saw new jobs come in well above expectations at 219k versus the consensus forecast of 186k. This along with the uptick we saw in the ISM manufacturing suggests that Friday’s Non-Farm payroll report will be solid.

- The AMEX Dollar Index (DXY) gained over +0.5% Monday through Thursday which is great for buying imports but…not so great for those companies selling outside the US.

On the not-so-great side:

- Back to the ISM Manufacturing report for July, the New Orders component is clearly on a downtrend, sitting at a 14-month low. To be fair, it has been above 60 for 15 consecutive months, something that has only happened two other times going back to WWII. While the level is still in solid territory, the 2.1 point decline is the largest setback since August 2016 and the 6-month moving average for New Orders has been steadily falling since February.

- The ISM Manufacturing report also showed that while production declined (-3.8 points), employment rose (+0.5 points) which means that productivity is declining – something I discussed Thursday morning on Cavuto Coast to Coast.

- Pending home sales were down 4% from last year.

- The Bureau of Labor Statistics Employment Cost Index for wages and salaries is now up 3.0% year-over-year, the fastest pace of the current expansion. Great for employees, not so great for investors because wages are rising faster than labor productivity plus inflation. Workers are taking home more, but businesses face margin pressures.

- Core capex spending, which is non-defense capital goods (excluding aircraft), was revised down and is trending down.

- Eurozone GDP was weaker than the expected 0.4% quarter-over-quarter increase, rising just 0.3%. That dropped the annual rate to 2.1% from the prior quarter’s 2.5%. While growth was weaker, inflation was higher at 2.1% versus expectations for 2.0%.

- China’s Markit manufacturing PMI came in below expectations and hit a 5-month low of 51.2 versus the prior 51.5. Non-manufacturing PMI was the slowest in a year. The trade battles may be having an impact as well with new export orders and new imports in contraction.

- The Markit Manufacturing PMI shows slowing growth in Japan, Taiwan and South Korean, (which is in contraction mode).

- Japan’s industrial production contracted, down -1.2% versus expectations for a 0.6% increase. South Korean’s Industrial Production did the same, falling -0.4% versus expectations for a +0.7% increase.

- Mexico’s GDP declined last quarter, falling -0.1% versus expectations for a +0.3%.

This week we saw indicators that inflation isn’t exactly taking off as many expected.

- The Fed’s preferred inflation measure, the core PCE (Personal Consumption Expenditure) Price index, came in weaker than expected at 1.9% (year-over-year) versus expectations for 2.0% while the headline US PCE inflation measure was 2.2% versus expectations for 2.3%. Inflation expectations declined on the news.

- The Employment Cost Index rose less than expected as well, up 0.6% (quarter-over-quarter) versus expectations for 0.7%.

- The Fed did not raise rates this week, in line with expectations. The market is still pricing in a more than 80% probability of a rate hike in September.

The Bottom Line for the Week

The US continues to outperform many other regions and the dollar continues to strengthen making our domestic stock market relatively more attractive. Job gains continue to beat expectations while inflation isn’t quite as bad as one would expect, but we are wary of just how much stocks are priced for perfection as we see margin pressures coming courtesy of the lack of available labor.

Next week is a pretty light one on the economic data front. We’ll get data on Job Openings, Consumer Credit, Producer and Consumer Price Indices and Wholesale Inventories as well as the Federal Budget. That last one will likely require a solid pour of Bordeaux. Have a great weekend!