Don’t Be Fooled By the Market, Several Uncertainties Loom Ahead

DOWNLOAD THIS WEEK’S ISSUE

The full content of The Monday Morning Kickoff is below; however downloading the full issue provides detailed performance tables and charts. Click here to download.

The first week of 2017 is now over. Granted it was a short one for the markets, but it saw the Dow Jones Industrial Average come ever so close to breaking through the 20,000 level.

Not to be left out, both the S&P 500 and the Nasdaq Composite Index climbed higher, with the S&P 500 up more than 1.5 percent and the Nasdaq up more than 2.5 percent. The later benefitted from the 2017 Consumer Electronic Show (CES 2017) conference last week, which featured the typical announcements that benefit our Connected Society, Asset-Lite and Disruptive Technology investing themes. This year was no different, given the show’s focus on new display technologies, digital assistants, and the Connected Car.

Those developments contributed to the technology-heavy Nasdaq breaking out of its mid-December range to close Friday at a new high. Meanwhile, the S&P 500 closed within points of its 52-week high, or at 17.1x expected 2017 earnings of $132.92 per share for the S&P 500. Now for a dash of perspective, that earnings forecast equates to 12 percent growth year-over-year — something we’ve not seen in quite some time.

As we’ll discuss further on, there are still a number of uncertainties hanging over our heads — ranging from Trump policies to additional dollar strengthening — all of which could end up weighing on that S&P 500 earnings outlook.

Our First Looks at the Jobs Equation for 2017

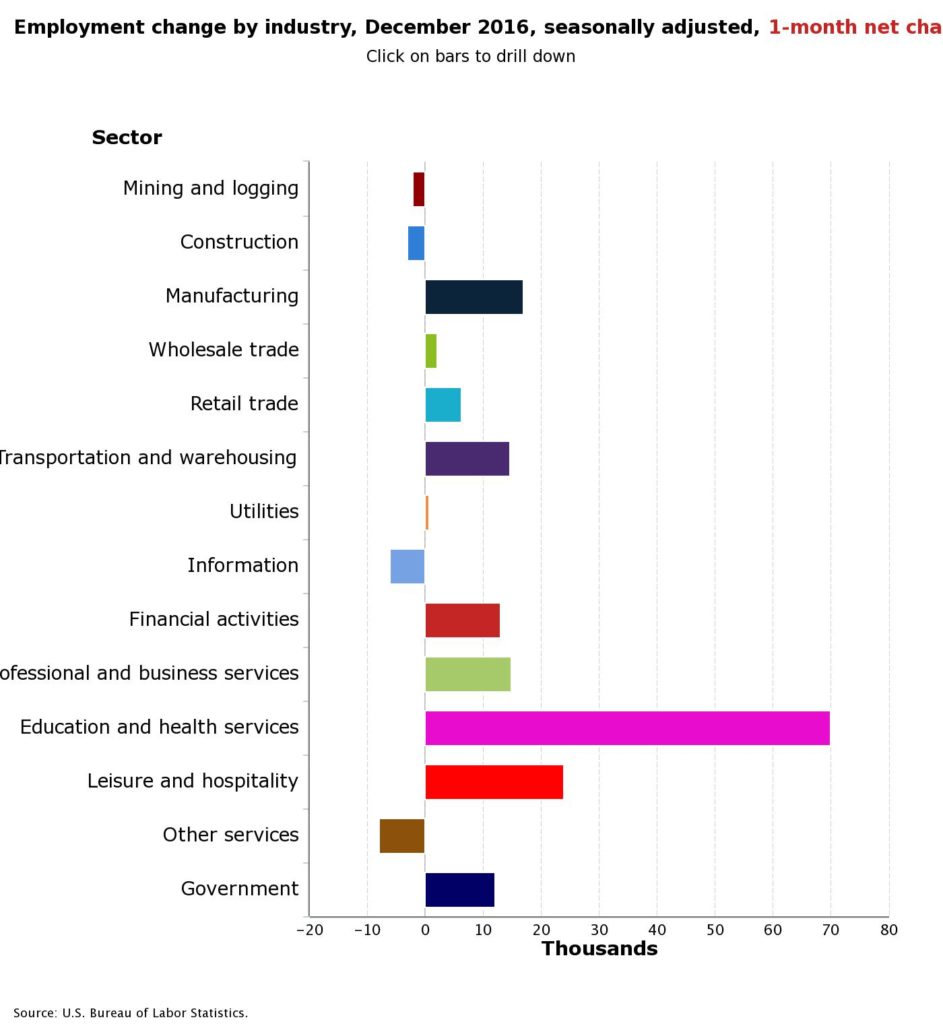

CES 2017 wasn’t the only center of news last week. Last Friday we received the first Employment Report of 2017 and, in a nutshell, it was weaker than expected. 156K jobs were created in December vs. the expected 176K jobs and much less than the upwardly revised 204K jobs (from prior 178k) created in November. By sector, the job gainers continued to be healthcare, (which bodes well for our Aging of the Population investment theme) social assistance, and food services — combined, those three categories accounted for 60 percent of new jobs created in December. Other job gainers included transportation, financial activities, manufacturing and business services.

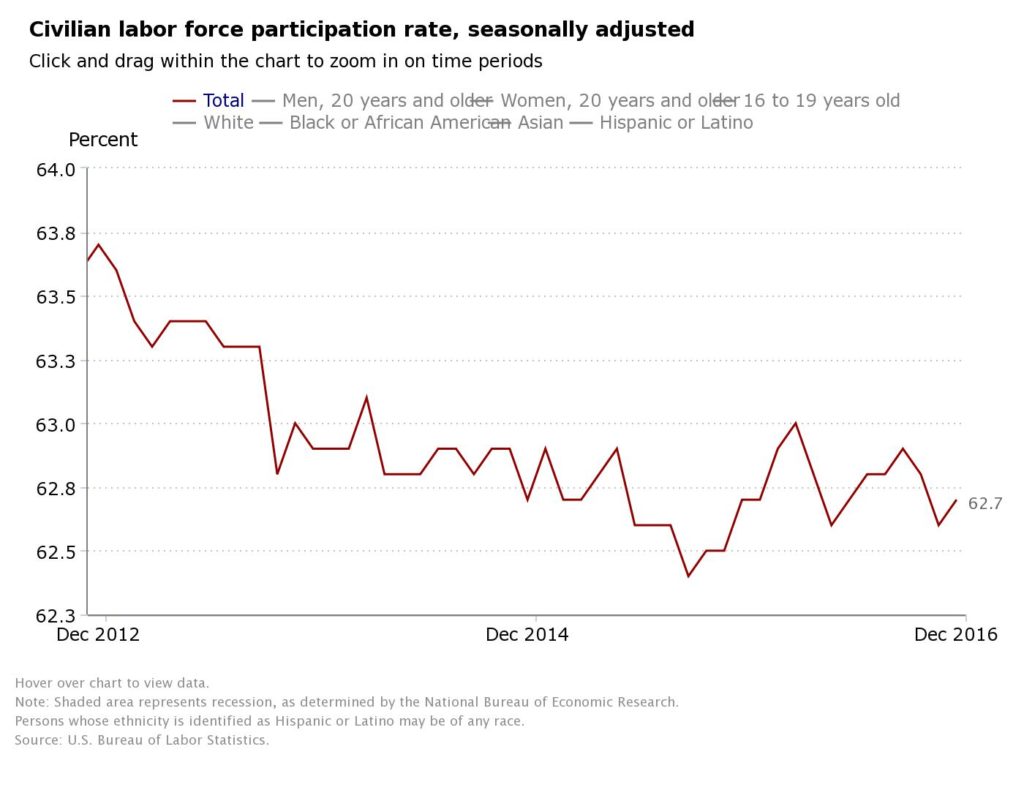

The big miss relative to expectations in the December report was with private sector jobs, which came in at 144K in December vs. 198K in November. The even bigger realization was the labor force participation ratio was little changed in December at 62.7 — and level that was essentially unchanged during all of 2016. The same goes for the employment-population ratio, which once again hovered near 59.7 percent. Those figures put a sobering view on the media touting the final month of President Obama’s term marked the 75th straight month that US employers added jobs, the longest such stretch on record since 1939.

In our view, those payroll-to-population and employment-to-population figures help explain the angst that led to the election of Donald Trump, as well as the post-election optimism and hope for the economy. While we are all for hope and enthusiasm, it’s never been a good move to invest based on those two things. As a sobering reminder, we have yet to hear the policies to be proposed by President-elect Trump, yet to know which policies will be passed and what the potential economic impact will be.

We’d also note this report tends to be volatile month-to-month, so we like to look the data from a longer-term perspective, like the twelve month moving average, to get a better idea of the longer-term trends. From that lens we can see that new job creation peaked back in February of 2015 and has been trending downward ever since. Not exactly something the media is reporting, and again, it helps explain the voter mindset this past November.

That Trump uncertainty, along with the fact that we are caught between the recent end to 2016 and the start of December quarter earnings season that begins shortly, means we are more or less in investing limbo.

We also can’t talk job creation without considering the Fed.

Yes, the Fed just raised interest rates in December for the second time in two years, but it also telegraphed it could raise those same interest rates three more times in 2017 — yes, not 1, not 2, but 3 times in a twelve month period. That’s a far more rapid pace than we’ve seen and it sent bank stocks like JPMorgan (JPM), Wells Fargo (WFC), Citigroup (C) and others soaring.

The big question is will the Fed actually raise interest rates that many times in 2017?

Remember the Fed talked quite a bit about boosting interest rates over the last two years, yet has only raised them twice during that time period, and that means while the Fed may like to hit its target of boosting rates three times in 2017, odds are it will remain not only data-dependent but also dependent on us waiting to understand the policies to be proposed by Trump and their impact. The recent notes from the Federal Reserve Open Market Committee meeting indicated that they are concerned that Trump may push through legislation and policies that are inflationary, which would shift the Fed into a more hawkish stance.

In other words, we’re back in the “will they, won’t they” Groundhog Day like nature of watching the Fed as we enter and move deeper into 2017. Pretty much, more of the same to what we saw in 2015 and 2016.

Let’s layer in even more data to add some perspective to Friday’s Employment Report.

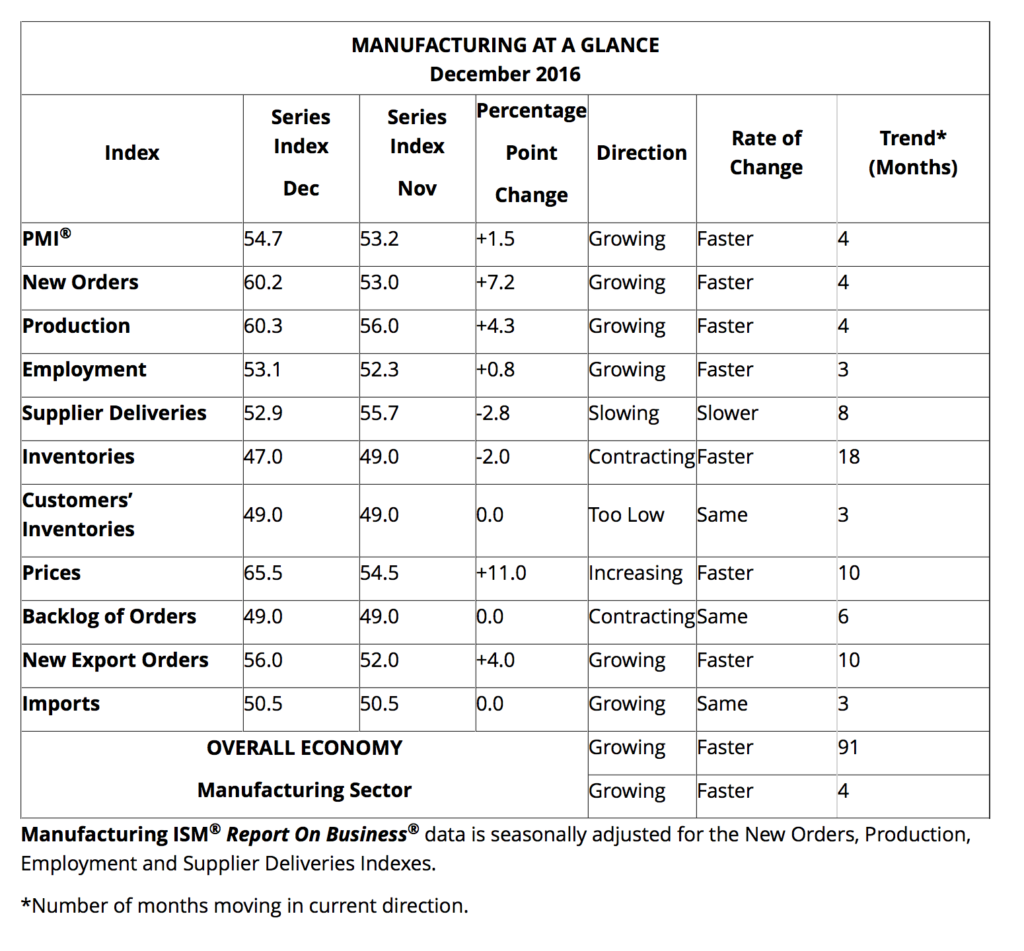

Early last week, we learned the Manufacturing economy was on stronger footing in December compared to November, per data from ISM and Markit Economics, but also per ISM the services economy slipped and ADP’s take on December job creation was less than expected.

It’s looking like the National Retail Federation may once again have overestimated consumer spending this past holiday shopping season. Following a 2.7 percent decrease in November and December comparable sales, Macy’s (M) announced additional layoffs as it begins to close 100 of its 730 locations. The same day, Kohl’s Corp. (KSS) announced that its stores also had disappointing holiday sales figures and did JCP Penny (JCP). Adding to the brick & mortar retail pain, Barnes & Noble (BKS), L Brands (LB) and Sears Holdings (SHLD) added their own disappointing holiday results.

How bad was it?

It was so bad that Sears, which is closing 150 Sears and Kmart locations, agreed to sell its Craftsman tool business to Stanley Black & Decker (SWK) for $900 million.

By comparison, Amazon (AMZN) shared that it shipped billions of packages this past holiday shopping season, and added even more Amazon Prime customers to its roster. Even as it offered a dour view on brick & mortar retail, Macy’s outgoing CEO Terry Lundgren did mention double-digit increases at its digital business. Even when Nike reported its quarterly earnings in mid-December it boasted a 46 percent year-over-year increase at nike.com.

We take all of those comments as positive indicators for the accelerating shift towards online and mobile commerce that is a key aspect of our Connected Society investing theme. Those comments also help explain why 5.8 million packages were expected to be returned during the first full week of January by US holiday shoppers, adding to the increased demand enjoyed by shippers such as FedEx (FDX) and United Parcel Service (UPS) from the shift to online and mobile shopping.

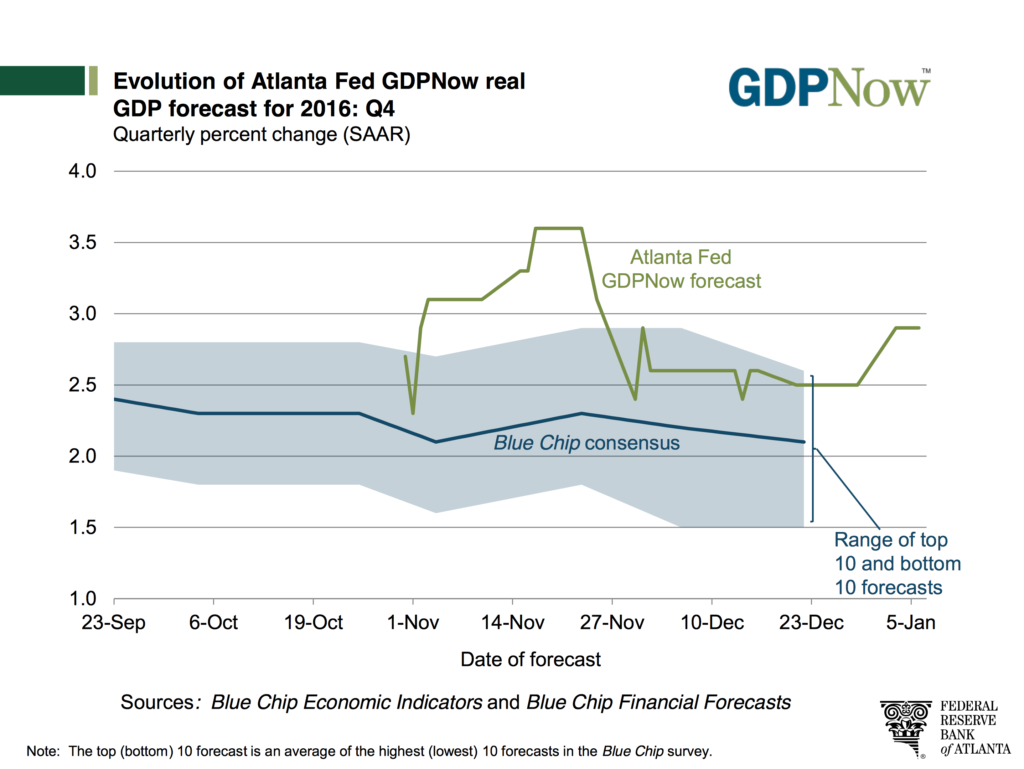

Factoring in the December Employment Report, the Atlanta Fed’s GDP Now reading still sat at 2.9 percent for 4Q 2016 as of last Friday vs. the third GDP print of 3.5 percent for 3Q 2016. As we’ve discussed in these pages during December, other firms are well below that 2.9 percent forecast for 4Q 2016, including the NY Federal Reserve and its NowCast publication. The Wall Street Journal’s latest Economic Forecasting Survey puts GDP at 2.3 percent for 4Q 2016as well as 1Q 2017 with a modest uptick to 2.4 percent in 2Q 2016. If Q4 comes in around 2 percent, we will have seen 1.6% GDP growth for the full year of 2016, a far cry from the 2.6% in 2015 and well below the pre-financial crisis long-term average going back to the 1930s of over 3 percent.

No matter how we slice it, the economy is shifting down a gear or two and faces some headwinds in the dollar, which could get worse should the Fed actually raise interest three times this year.

Putting it all together reminds us that despite the enthusiasm and hope that has overtaken the stock market about President-elect Trump jumpstarting the economy, we still have to navigate through the December quarter and most likely at least the first half of 2017 before his policies, whatever they windup being, start to have an impact on the economy. Given warnings from retailers, as well as cautionary comments from Honeywell (HON) and Adobe Systems (ADBE) over the potential impact of continued dollar strength in 2017, there are reasons to look at the recent market moves and think it has gotten a bit ahead of itself, with the forward price-to-earnings ratio on the S&P 500 at levels not seen since 2002, which was quickly followed by a 30 percent decline in the market.

As Tematica’s Chief Macro Strategist Lenore Hawkins pointed out during a visit with Varney & Company on Fox Business last Friday, the market is not pricing in the level of political risk we face this year, with elections coming up in Germany, France, the Netherlands and potentially Italy. Those elections, that include the threat of euro-skeptics Marine Le Pen in France and the Five Star Movement in Italy gaining political momentum, could lead to serious weakening with the euro.

A fall in the euro currency would strengthen the dollar significantly, which would weigh on not only dollar-denominated commodities, but also export business for US companies. In other words, the current currency headwind could get even stronger.

If we get more of the same commentary from Honeywell, Adobe, Macy’s, Sears, JC Penney, Kohls’s and even Fattening of the Population thematic contender Sonic Corp. (SONC) that shared it saw a “sluggish consumer landscape” in the December quarter, we could very well see the market pullback from current levels as the flow of December quarter earnings reports heat up. Should that come to pass, on the back of reset expectations, odds are stocks will be at much fall to more favorable prices than they stand now and that is likely to offer a buying opportunity.

Gearing Up for a Full 5 Days of Trading & Data

We’ll get several clues this week as to whether our pullback expectations are likely as we dip into December quarter earnings with industrial companies Alcoa (AA) and WD40 (WDFC) as well as Cashless Consumption contender Global Payments (GPN). Given the year-end strength in our Economic Acceleration/Deceleration investing theme and the number of industries that it touches, we’ll be breaking down Alcoa’s market commentary and outlook.

Mid-week we get a look at Cash-strapped Consumer company SuperValu (SVU) and Connected Society building block company Taiwan Semiconductor (TSM) and potential Tooling & Re-Tooling company Staffing 360 (STAF). Closing out the week is a financial smorgasbord on Friday with JPMorgan Chase (JPM), Wells Fargo (WFC), Bank of America (BAC), Blackrock (BLK) and PNC Financial Services (PNC), all reporting December quarter results. Inside those reports, we’ll be looking to hear about the pace of new loan activity as well as their view on the overall economy in 2017.

Reading between those lines, you likely realized that, yes, this week we’re back to a full 5 days of market activity — the first in two weeks! That dribble of earnings reports aside, we’ve got a full plate of economic data. Among the various reports, the two standouts are likely to be the December PPI, which will be watched closely by the Fed, and December Retail Sales reports. Given recent comments from Macy’s (M) and other retailers, we’re not expecting any upside surprises in the December Retail Sales Report. We will be digging into it to for data relative to our Cash-strapped Consumer, Connected Society and other investment themes.

This week we also have the 35th Annual JPMorgan Healthcare Conference 2017, the Needham and Company’s 19th Annual Growth Conference as well as the North American International Auto Show of Detroit 2017. We expect there to be much fodder for our Aging of the Population investment theme at the JPMorgan conference, while the auto show is likely to result in several announcements pertaining to driver assisted and driverless technologies. Odds are the recent announcement that AT&T (T) is partnering with Honda Motor (HMC) to bring 4G LTE connectivity into its vehicles as well as the deals announced by both Amazon (AMZN) and Alphabet (GOOGL) to bring their digital assistants — Echo and Google Home — to cars from Hyundai, Ford (F) and Chrysler (FCAU), is just the start of the Connected Car news flow this week.

Yep, it’s going to be a busy one, but be sure to enjoy the week and we’ll be back with you next Monday with the next MMKO.

Hello and welcome to the 7th volume of Thematic Signals! 2023 has only just started but investors are staring down what is likely to be a challenging December quarter earnings season laced with recession fears, structural changes in the economy, across demographics, technology, and consumer behavior all continue to unfold. While some folks continue to […]

Traditionally, data privacy and the safeguarding of digital identity products and services have been lumped within the broader scope of Cybersecurity. Tematica recently launched the Tematica Bita Data Privacy and Digital Identity Index. It is our view that traditional cybersecurity is increasingly focused solely on the protection of large stores of data. Protecting personal privacy and […]

Happy Holidays and Merry Christmas readers! While many are busy couch surfing or braving brick & mortar stores to get ready for the coming holidays and gift-giving season, we continue to be overwhelmed with confirming data points for our investment strategies. That said, this week’s Thematic Signals is likely to be the last one of […]

Hey folks, as you likely suspect we at Tematica do a lot of leg work and deep dives when developing our investment themes and refreshing our thematic mosaic. This means that in addition to scouring financial filings, company presentations, and earnings transcripts, we also chat with company management, thought leaders, and other industry movers and […]

This conversation is provided for informational purposes only and is not an offer or solicitation to buy or sell any securities. Tematica Research was compensated by a third party to conduct this interview. The information described herein is taken from sources that we believe to be reliable, but we do not guarantee the accuracy and completeness of […]

While we at Tematica tend not to focus on the precise figures for forecasts that span more than a year or two out, the direction of EV adoption and therefore the need for additional EV charging stations per KPMG’s findings serves as a solid multi-year confirmation point for the Cleaner Transportation aspect our Cleaner Living […]