Liquidity Trumps Fundamentals

The market has been back in risk-on mode but with some strange internals as well as an ongoing disconnect with fundamentals. It has priced in a joyous cornucopia of Goldilocks assumptions:

- A return to global central bank liquidity and price supports

- A reversal of China’s deleveraging campaign with an abundance of stimulus measures

- A peaceful and prosperous end to global trade wars

- An elegant resolution to Brexit

- Never mind India and Pakistan

The Party is Back On, But the Music Sounds Off

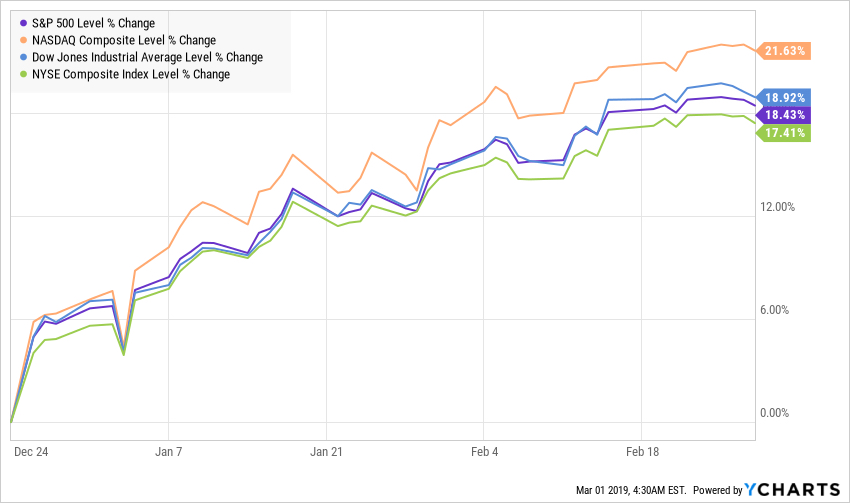

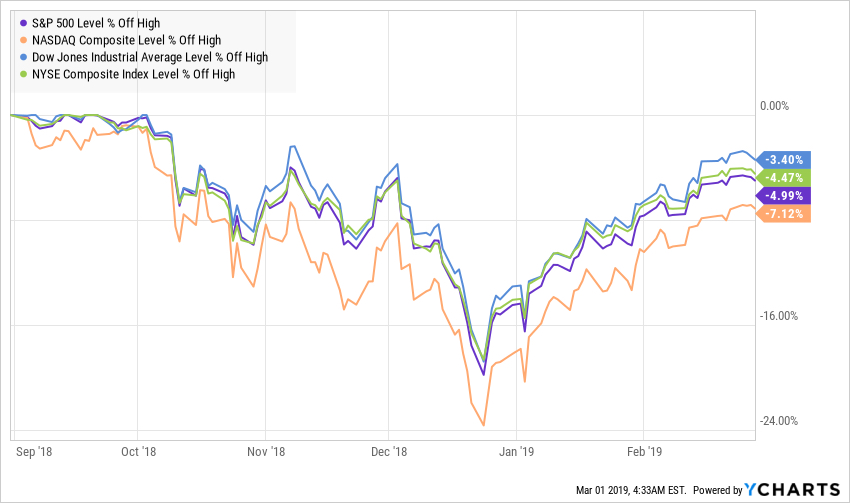

Heading into the last month of the quarter, let’s review what we’ve seen over the past few months. Just over 50 days ago the Nasdaq was in a bear market, but in the past two months it has shot up over 21% to sit about 7% below the September high and is currently above both its 50-day and 200-day moving averages which is typically viewed as being in a solid uptrend. As of the US market’s close on Thursday the Dow Jones Industrial Average was up nearly 19% from the December low (3.4% below its high), the S&P 500 up nearly 19% (5.0% below its high) and the broader NYSE Composite Index up just under 18% (4.5% below its high).

All the major indices remain below their Fall 2018 highs but are within range. However, upward momentum has stalled recently with the majority of the major US indices relatively flat or down since last Friday. This looks to be the fourth failed attempt by the S&P 500 to break 2,800 in the past four months indicating a significant overhead resistance level.

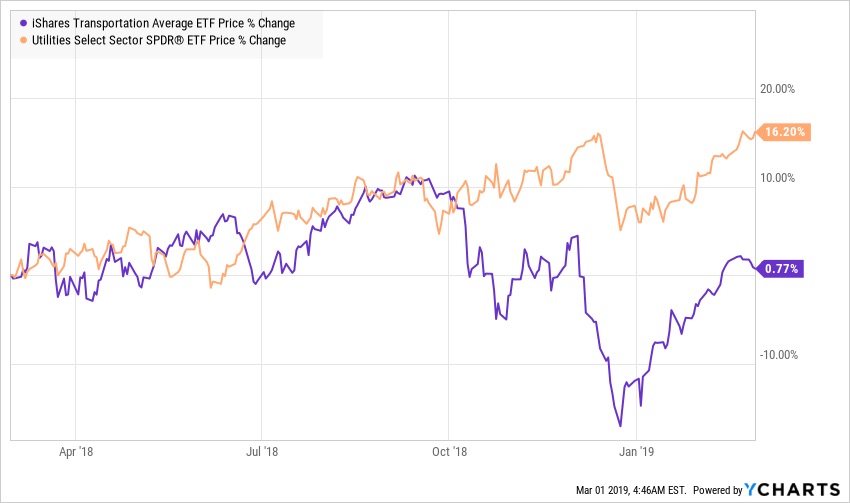

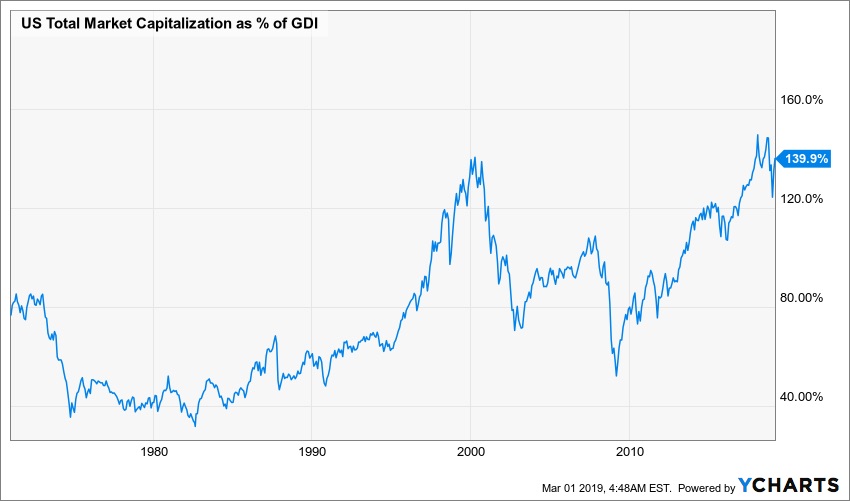

As we can observe in the chart above, the domestic stock market indices experienced the worst December since 1931 followed by the best January since 1987, leaving many with a general sense of unease. Let me be clear, these moves are not indicative of market normalcy. Something is very different, and it doesn’t feel quite right to me or to Tematica’ Chief Investment Officer Chris Versace. For example, it doesn’t feel like a normal bull market when Utilities have outperformed transports over the past year by over 15%. It doesn’t feel like a normal market when a growing number of companies are slashing their dividends while share prices continue to move upwards.

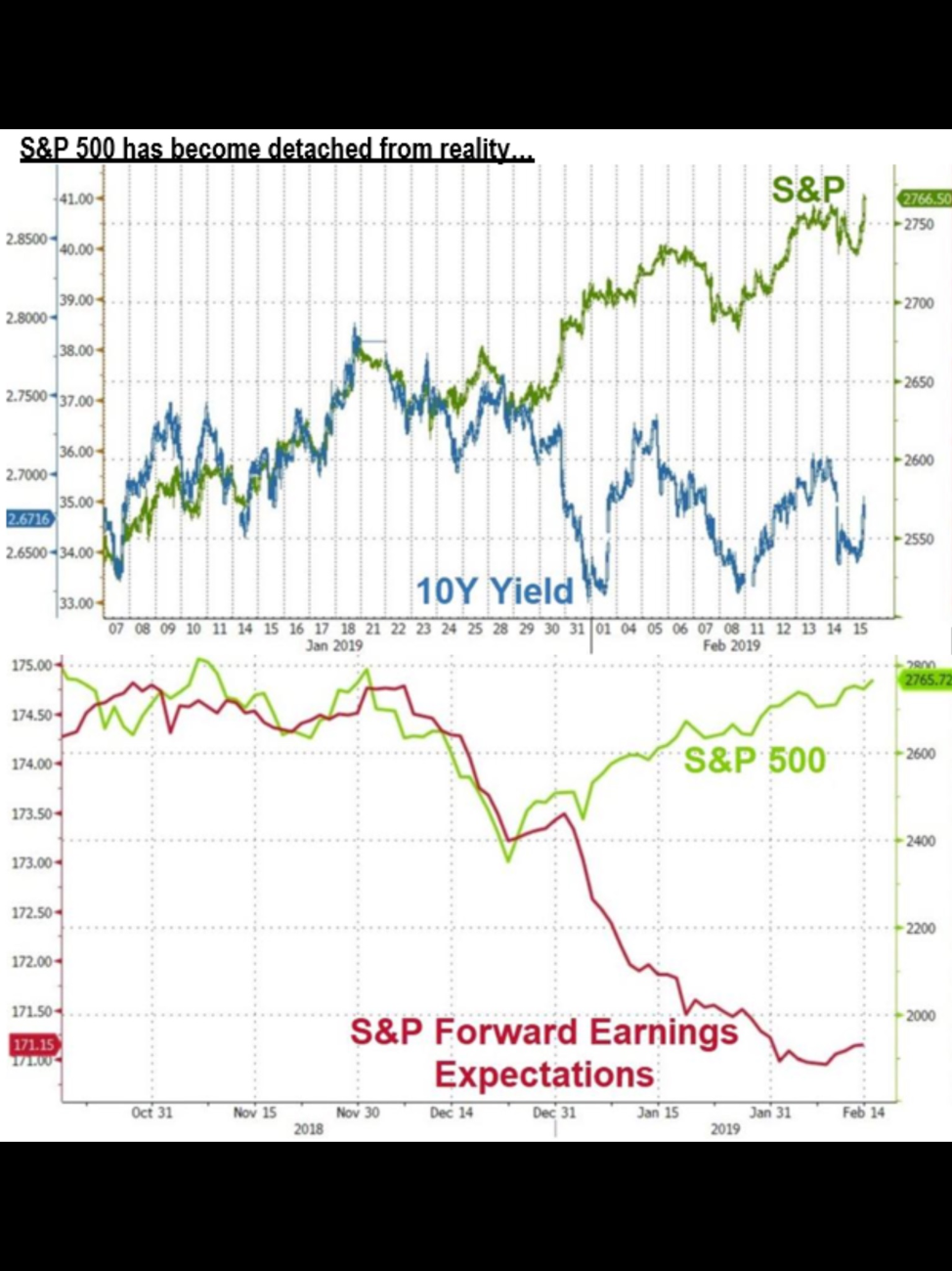

Then there is the disconnect with earnings and yields. As of the end of last week, 89% of companies in the S&P 500 had reported results for the December quarter with 69% reporting EPS above estimates, below the 5-year average. Analyst expectations for 2019 are for a decline in first quarter earnings of -2.7% with a meager 0.7% increase in the second quarter and just 2.2% growth in the third. For 2019 in full, the S&P 500 group of companies are now only expected to grow their collective EPS by 4.7%, more than 50% below forecasted levels at the start of the December quarter, yet share prices are rising.

We’ll also just have to ignore that the Citi Global Economic Surprise Index is right around where it was at the December market lows and has now been below zero for over 230 days, a record exceeded only during the financial crisis. The nominal manufacturing and non-manufacturing ISM has declined for the past 3 consecutive months and sits 13% below where it was when the 2008 recession began and is 19% below the 2000 recession.

In the battle between fundamentals and central bank liquidity so far, the bankers are winning big.

While this last one is certainly utterly useless as far an indicator of when a market may turn, it does put the current state of the stock market into perspective. The last time the market was in such heady territory the overall, (in the dotcom mania of 1999-2000) returns for the stock market for the following decade were quite grim with positive returns more dependent on specific asset selection than overall market bullishness – one of the reasons we are so focused on powerful long-term investment themes driven by structural changes.

The stock market rally thus far in 2019 hasn’t been just in the US as European stocks are enjoying their best start to a year since 2015, despite slowing economies and the mess of Brexit. The Stoxx Europe 600 has gained over 10% so far this year, gaining nearly as much as the S&P 500. We’ll also just have to ignore that Europe’s largest bank, HSBC, reported results earlier this month that missed analysts’ expectations with the bank’s CEO stating that revenues “collapsed” at the end of the year. There I go again with fundamentals!

Taking a Dip Back in that Central Bank Pool

While the markets have cheered the Fed’s cessation of its rate hike plans, it is worth keeping in mind that the US Federal Reserve has never stopped tightening with a funds rate this low. More than 10 years after the depths of the financial crisis and the economy cannot withstand getting near normal interest rates.

“And so, you know, when I think about the projection, I’m projecting 2 percent growth right now for 2019. That’s a number that is quite a bit slower than last year, which looks like – you know, barring any big surprises in the fourth quarter looks to come in around 3 percent. So that would be a percentage point difference in last year and 2019. That’s a pretty substantial slowdown…..If the economy evolves as I just said I expect it to – 2% growth, 1.9 % inflation, no sense that it’s going up, no sense that we have any acceleration – then I think the case for rate increases is not there. “

– Mary Daly, head of San Francisco Fed in WSJ interview

The markets are embracing the Fed’s far more dovish view on rate hikes that is driven by the Fed’s concern the US economy will return to its significantly weaker growth rate. That doesn’t sound like a great reason to break out the bubbly. We will be watching for signs that the better-than-expected fourth quarter GDP growth of 2.6% gives the Fed reason to believe higher rates are possible knowing that they’d like to get rates up higher to have more arrows in the quiver for the inevitable downturn. Given the data of late, however, the odds at least in the near-term for an additional rate hike seem rather low.

One of the major challenges facing the Fed when it comes to raising rates is part of our Aging of the Population investing theme – the reality that Social Security is expected to run out of money in 12 years, according to the Congressional Budget Office. The problem with raising rates is that the US is running exceptionally large fiscal deficits. Higher rates mean more of the budget goes to interest expense, bringing the problems with Social Security even more quickly.

Central banks around the world continue to feel the need to support asset prices after one of the longest bull markets in history and one of the longest periods in history without a recession, (in part because of the rampant levels of deficit spending and unfunded payables to their nation’s retirees). Call me crazy, but that doesn’t sound fundamentally bullish.

“There might be scope for another TLTRO.”

– European Central Bank Board member (and one of Mario Draghi’s possible successors when the latter’s term runs out on October 31) when discussing the idea of issuing new multi-year cheap loans to banks when the current Targeted Long-Term Refinancing Operation (TLTRO) nears its repayment date in 2020.

Once again investors have been taught that dips are a buying opportunity and implementing portfolio protection can go very wrong. Investors have been getting this lesson pounded into them for over 10 years now with many in the markets never having experienced a sustained market downturn. That is worrisome if you believe at all in reversion to the mean. Equity price growth has grossly outpaced economic growth – how long can that last? In today’s market to not participate is to seriously risk missing out, but just when do we pay the piper and are enough market participants paying attention to the rising risks?

While investors are keeping their eyes on the markets, our Middle-Class Squeeze investment theme continues to illustrate that all is not rosy for many as is evidenced by the rising populism around the world.

China’s Policy Shifts into Reverse

Last year China was working to deleverage its highly leveraged economy, just how highly leveraged is up for debate as its leadership isn’t exactly keen on transparency. China’s leadership is eternally under pressure to keep economic growth robust, making the nation one of the participants in our New Global Middle-Class investment themes.

The deleveraging efforts, the trade war with the US and the overall slowing global economy led to China’s economy growing at the slowest pace in nearly 30 years in 2018. China’s February manufacturing PMI fell to its weakest level since early 2016 and was the third consecutive month of contraction. Export orders are now slowing at the fastest pace since the global financial crisis and imports PMI is at the lowest level in over a decade.

With all that weakness China has reversed course on its deleveraging, but not everyone is on board with efforts that led to record lending of $530 billion in new loans in January alone. We saw a rare public row between the central bank and Premier Li Keqiang with the former stating clearly that it will continue efforts to deleverage while the latter argued that a sharp rise in rates creates new potential risks.

Both China and the US, the two largest economies in the world, have witnessed public rows between national leaders and central banks concerning risks around leverage and economic weakness.

The markets are unsurprisingly placing their bets with rising liquidity as Chinese stocks enjoyed their best day since 2015 earlier this week. The biggest concern regarding financial stability and future economic growth potential is China’s ballooning debt. Its official corporate debt level is among the highest in the world and its public debt is equally astounding.

But then who cares about debt these days…

Trade Wars Running Hot and Cold

On the China trade front, things are looking better as this week US Trade Representative Robert Lighthizer stated that the US is (at least for now) shelving its threat to raise tariffs to 25% on $200 billion of Chinese good. President Trump’s willingness to walk out on talks with North Korea’s Kim Jung Un this week may have been a signal to China that he could also walk out on President Xi if he doesn’t get what he wants. I wouldn’t want to place too many bets on this one working out smoothly from this point onwards. And let’s remember that should we get a trade deal in the coming days or weeks, investors will need to look past the headlines and dig into the details of the agreement to ascertain its true impact.

While the upcoming talks between the US and China are getting most of the headlines, as the Wall Street Journal put it, “America car buyers are facing sticker shock as President Trump weights new tariffs on imported vehicles and auto parts.” Even buyers of domestically produced cars would be affected as between 40% and 50% of the average US-built car uses imported components, according to the Center for Automotive Research. Potentially a second shoe to drop for auto companies following the data concerning falling auto loan demand that I shared just a few weeks ago.

The reality is that thousands and thousands of companies in Europe alone have been bracing themselves, (which means for many cost-cutting programs) for the ongoing impacts of the US-China trade war, fallout from rising populism in the Eu and the mind-boggling mess that Brexit has become. In Germany, long the economic engine of the EU, the government expected GDP growth to slow to just 1% in 2019.

Brexit A Mess of Historical Proportions

When it comes to Brexit, the mess just keeps growing. Long, long, long story short, essentially the divorce technically has a hard and fast move-out date at the end of March yet there has been no agreement on the terms of the divorce. There is talk of another referendum which could possibly reverse the 2016 vote, but that would be so very un-British to go back on a decision like that and Prime Minister Theresa May has said this is a no-go for her. This mess has left companies from the tiny local grocer to the major multi-national without any guidance on how their businesses will be affected in just one month’s time. The impact has the potential to be brutal with estimates that the UK’s economy, with a hard exit, could contract on the order of nearly 10%. This is something without any precedent in modern global politics and is a serious headwind to growth in the region. Perhaps the Brits will be wooed back into the European Union by the Breunion Boys – do yourself a favor and click on that link, you’ll thank me.

While we are on the topic of messes in Europe, an aspect of our Safety and Security investing theme is on display as Facebook (FB) faces yet another privacy investigation, this time 10 investigations lead by Ireland’s privacy regulator concerning potential violations of European Union privacy law.

India and Pakistan Ignite

A tailwind for our Safety and Security investing theme is rising global tensions as economies around the world struggle to maintain growth rates necessary to keep their populations feeling good about the future. When people have little hope for a better economic future, violence tends to follow whether it be against a neighboring nation or other members of their own society.

The US this week urged India and Pakistan to refrain from further military action as international pressure is building to de-escalate the most serious flare-up between the long-standing rivals in decades with fighter jets from both nations being shot down. We have not had such tit-for-tat air strikes between the two nations since 1971. We’ll continue to watch this potential powder keg of a situation, which if it escalates further it could very well move to the forefront of investor concerns.

The Bottom Line

Equity markets have once again diverged materially from fundamentals as the perception of the central bank put from the world’s biggest economies overrides fundamentals. I’ve been admittedly surprised by how long this has been going on and how wide the divergence has become, but we are seeing now seeing substantial overhead resistance level for the S&P 500 at a time when challenging fundamentals are growing.