As 5G fires up across the nation and beyond, this chip-maker will likely be called on to let phones connect to new and old generations of networks.

As the smartphone market has matured, it has become increasingly tied to replacement demand.

Look at these statistics: As of December 2019, there are 5.175 billion unique mobile subscribers across the globe, according to the Global System for Mobile Communications, or GSM Association. As surprising as it may sound, the last big quarter for smartphone shipments was the fourth one in 2016. So, despite the seasonal pattern for stronger smartphone sales in the back half of the year, the 1.4 billion units shipped in 2018 was relatively unchanged year-over-year. Prospects for shipments in 2019 also point to modest growth year-over-year.

As we move through 2020, mobile operators will light up their next generation 5G networks that will likely be…

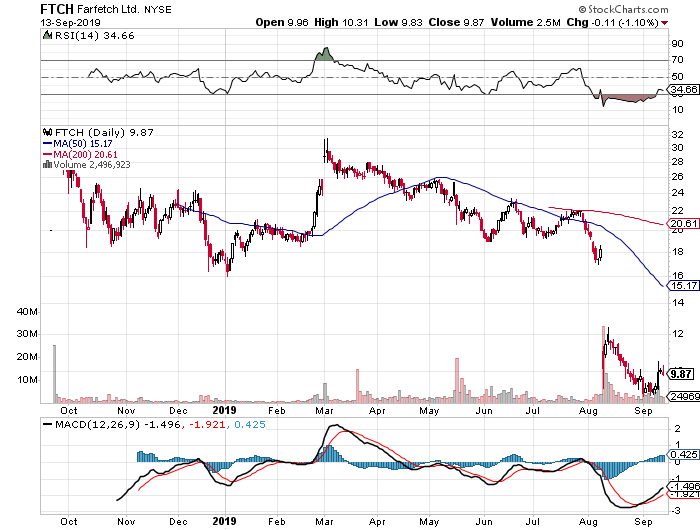

Farfetch Limited (FTCH) – A fashionable Living the Life Thematic Leader

Digital Lifestyle – The August Retail Sales confirms the adoption continues

Economics & Expectations

The Fed Takes Center Stage Once Again

As we saw last week, the primary drivers of the stock market continue to be developments on the U.S.-China trade front and the next steps in monetary policy. As the European Central Bank stepped up its monetary policy loosening, it left some to wonder how much dry powder it had remaining should the global economy slow further and tip into a recession. Amid those concerns, along with some discrepancy among reports that President Trump would acquiesce to a two-step trade deal with China, stocks finished last week with a whimper after rebounding Wednesday and Thursday.

We continue to see intellectual property and national security as key tenets in negotiating a trade deal with China. We will watch as the lead up to October’s next round of trade negotiations unfolds. Given the Fed’s next two-day monetary policy meeting that begins on Tuesday and culminates with the Fed’s announcement and subsequent press conference, barring any new U.S.-China trade developments before then, it’s safe to say what the Fed says will be a key driver of the stock market this week.

Leading up to that next Fed press conference, we will get the August data for Industrial Production and Housing Starts as well as the September Empire State Manufacturing Index. Paired with Friday’s August Retail Sales report and last Thursday’s August CPI report, that will be some of the last data the Fed factors into its policy decision.

Per the CME Group’s FedWatch tool, the market sees an 82% probability for the Fed to cut interest rates by 25 basis points this week with possibly one more rate cut to be had before we exit 2019. Normally speaking, parsing the Fed’s words and Fe Chair Powell’s presser commentary are key to getting inside the central bank’s “head,” and this will be especially important this time around. One of our concerns has been the difference between the economic data and the expectations it is yielding in the stock market. Should the Fed manage to catch the market off guard, odds are it will give the market a touch of agita.

On the earnings front

there are five reports that we’ll be paying close attention to this week. They are Adobe Systems (ADBE), Chewy (CHWY), FedEx (FDX), General Mills (GIS) and Darden Restaurants (DRI). With Adobe, we’ll be examining the rate of growth tied to cloud, an aspect of our Disruptive Innovators investing theme. With Darden we’ll look to see if the performance at its full-service restaurants matches up with the consumer trade-down data being reported by the National Restaurant Association. That data has powered shares of Cleaner Living Thematic Leader and Cleaner Living Index resident Chipotle Mexican Grill (CMG) higher of late, bringing the year to date return to 82% vs. 20% for the S&P 500. Chewy is a Digital Lifestyle company that is focused on the pet market serving up food, toys, medications and other pet products. Fedex will not only offer some confirmation on the digital shopping aspect of our Digital Lifestyle investing theme it will also shed some light on the global economy as well.

Farfetch Limited – A fashionable Living the Life Thematic Leader

In last week’s issue, I mentioned that I was collecting my thoughts on Farfetch Limited (FTCH), a company that sits at the intersection of the luxury goods market and digital commerce. Said thematically, Farfetch is a company that reflects our Living the Life investment theme, while also benefitting from tailwinds of our Digital Lifestyle theme. Even though the company went public last year, it’s not a household name even though it operates a global luxury digital marketplace. As the shares have fallen over the last several weeks, I’ve had my eyes on them and now is the time to dip our toes in the water by adding FTCH as a Thematic Leader.

Farfetch Provides Digital Shopping to the Exploding Global Luxury Market

Farfetch is a play on the global $100 billion online luxury market with access to over 3,200 different brands across more than 1,100 brand boutique partners across its platform. With both high-end and every-day consumers continuing to shift their shopping to online and mobile platforms, we see Farfetch attacking a growing market that also has the combined benefit of appealing to the aspirational shopper and being relatively inelastic compared to mainstream apparel.

Part of what is fueling the global demand for luxury and aspirational goods is the rising disposable income of consumers in Asia, particularly China. According to Hurun’s report, The Chinese Luxury Traveler, enthusiasm for overseas travel shows no signs of abating, with the proportion of time spent on overseas tourism among luxury travelers increasing 5% to become 70% of the total. Cosmetics, (45%), local specialties (43%), luggage (39%), clothing and accessories (37%) and jewelry (34%) remain the most sought — after items among luxury travelers. High domestic import duties and concerns about fake products contribute to the popularity of shopping abroad.

It should come as little surprise then that roughly 31% of FarFetch’s 2018 revenue was derived from Asia-Pacific with the balance split between Europe, Middle East & Africa (40%) and the Americas (29%). At the end of the June 2019 quarter, the company had 1.77 million active customers, up from 1.35 million exiting 2018 and 0.9 million in 2017. As the number of active users has grown so too has Farfetch’s revenue, which hit $718 million over the 12 months ending June 2019 compared to $602 million in all of 2018 and $386 million in 2017.

Farfetch primarily monetizes its platform by serving as a commercial intermediary between sellers and end consumers and earns a commission for this service. That revenue stream also includes fees charged to sellers for other activities, such as packaging, credit-card processing, and other transaction processing activities. That business accounts for 80%-85% of Farfetch’s overall revenue with the balance derived from Platform Fulfillment Revenue and to a small extent In-Store Revenue.

New Acquisition Transformed Farfetch’s Revenue Mix

In August, Farfetch announced the acquisition of New Guards Group, the Milan-based parent company of Off-White, Heron Preston and Palm Angels, in a deal valued at $675 million. New Guards will serve as the basis for a new business segment at Farfetch, one that it has named Brand Platform. Brand Platform will allow Farfetch to leverage New Guards’ design and product capabilities to expand the reach of its brands as well as develop new brands that span the Farfetch platform. For the 12-month period ending April 2019, the New Guards portfolio delivered revenue of $345 million, with profits before tax of $95 million. By comparison, Farfetch posted $654 million in revenue and an operating loss of $183 million over that time frame.

Clearly, another part of the thought behind acquiring New Guards and building the Brand Platform business is to improve the company’s margin and profit profile. And on the housekeeping front, the $675 million paid for New Guards will be equally split between cash and stock. Following its IPO last year, Farfetch ended the June quarter with roughly $1 billion in cash and equivalents on its balance sheet.

In many ways what we have here is a baby Amazon (AMZN) that is focused on luxury goods. Ah, the evolution of digital shopping! And while there are a number of publicly traded companies tied to digital shopping, there are few that focus solely on luxury goods.

Why Now is the Time to Add FTCH Shares

We are heading into the company’s seasonally strongest time of year, the holiday shopping season, and over the last few years, the December quarter has accounted for almost 35% of Farfetch’s annual sales. With the company’s active user base continuing to grow by leaps and bounds, that historical pattern is likely to repeat itself. Current consensus expectations have Farfetch hitting $964 million in revenue for all of 2019 and then $1.4 billion in 2020.

At the current share price, FTCH shares are trading at 1.6x expected 2020 sales on an enterprise value-to-sales basis. The consensus price target among the 10 Wall Street analysts that cover the stock is $22, which equates to an EV/2020 sales multiple of near 3.5x when adjusting for the pending New Guards acquisition. As we move through this valuation exercise, we have to factor into our thinking that Farfetch is not expected to become EBITDA positive until 2021. In our view, that warrants a bit of haircut on the multiple side and utilizing an EV/2020 sale multiple of 2.5x derives our $16 price target.

Despite that multiple, there is roughly 60% potential upside to that target vs. downside to the 52-week low of $8.82.

We are adding FTCH shares to the Thematic Leaders for our Living the Life investing theme.

A $16 price target is being set and we will wait to put any sort of stop-loss floor in place.

Digital Lifestyle – The August Retail Sales confirms the adoption continues

One of last week’s key economic reports was the August Retail Sales report due in part to the simple fact the consumer directly or indirectly accounts for two-thirds of the domestic economy. Moreover, with the manufacturing and industrial facing data – both economic and other third-party kinds, such as truck tonnage, railcar loadings and the like – softening in the June quarter, that quarter’s positive GDP print hinged entirely on the consumer. With domestic manufacturing and industrial data weakening further in July and August, the looming question being asked by many an investor is whether the consumer can keep the economy chugging along?

In recent months, I’ve voiced growing concerns over the spending health of the consumer as more data suggests a strengthening tailwind for our Middle-Class Squeeze investing theme. Some of that includes the Federal Reserve Bank of New York’s latest Household Debt and Credit Report, consumer household debt balances have been on the rise for five years and quarterly increases continue on a consecutive basis, bringing the second quarter 2019 total to $192 billion. Also a growing number of banks are warning over rising credit card delinquencies even as the Federal Reserve’s July Consumer Credit data showed revolving credit expanded at its fastest pace since November 2017.

Getting back to the August Retail Sale report, the headline print was a tad better than expected, however once we removed auto sales, retail sales for the month were flat. That’s on a sequential basis, but when viewed on a year over year one, retail sales excluding autos rose 3.5% year over year. That brought the year over year comparison for the three-months ending with August to up 3.4% and 1.5% stronger than the three months ending in May on the same basis.

Again, perspective can be illuminating when looking at the data, but what really shined during the month of August was digital shopping, which rose 16.0% year over year. That continued strength following the expected July surge in digital shopping due to Amazon Prime Day and all the others that looked to cash in on it led year over year digital shopping sales to rise 15.0% for the three months ending in August.

Without question, this aspect of our Digital Lifestyle investing theme continues to take consumer wallet share, primarily at the expense of brick & mortar retailers, especially department stores, which saw their August retail sales fall 5.4%. That continues the pain felt by department stores and helps explain why more than 7,000 brick & mortar locations have shuttered their doors thus far in 2019. Odds are there is more of that to come as consumers continue to shift their dollar purchase volume to online and mobile shopping as Walmart (WMT), Target (TGT) and others look to compete with Amazon Prime’s one day delivery.

For all the reasons discussed above, Amazon remains our Thematic King as we head into the seasonally strong holiday shopping season.

Elliot Management gets active in AT&T, but its prefers Verizon?

California approves a bill that changes how contract workers are treated

Volkswagen set to disrupt the electric vehicle market

I’m going to deviate from the usual format we’ve been using here at Tematica Investing this week to focus on some of what’s happening with Select List residents Apple (AAPL) and AT&T (T) this week as well as one or two other things. The reason is the developments at both companies have a few layers to them, and I wanted to take the space to discuss them in greater detail. Don’t worry, we’ll be back to our standard format next week and I should be sharing some thoughts on Farfetch (FTCH), which sits at the crossroads of our Living the Life, Middle Class Squeeze and Digital Lifestyle investing themes, and another company I’ve been scrutinizing with our thematic lens.

Apple’s 2019 iPhone event – more meh than wow

Yesterday, Apple (AAPL) held its now annual iPhone-centric event, at which it unveiled its newest smartphone model as well as other “new”, or more to the point, upgraded hardware. In that regard, Apple did not disappoint, but the bottom line is the company delivered on expectations serving up new models of the iPhone, Apple Watch and iPad, but with only incremental technical advancements.

Was there anything that is likely to make the average users, not the early adopter, upgrade today because they simply have to “have it”?

Not in my view.

What Apple did do with these latest devices and price cuts on older models that it will keep in play was round out price points in its active device portfolio. To me, that says CEO Tim Cook and his team got the message following the introduction of the iPhone XS and iPhone XS Max last year, each of which sported price tags of over $1,000. This year, a consumer can scoop up an iPhone 8 for as low as $499 or pay more than $1,000 for the new iPhone 11 Pro that sports a new camera system and some other incremental whizbangs. The same goes with Apple Watch – while Apple debuted a new Series 5 model yesterday, it is keeping the Series 3 in the lineup and dropped its price point to $199. That has the potential to wreak havoc on fitness trackers and other smartwatch businesses at companies like Garmin (GRMN) and Fitbit (FIT).

Before moving on, I will point out the expanded product price points could make judging Apple’s product mix revenue from quarter to quarter more of a challenge, especially since Apple is now sharing information on these devices in a more limited fashion. This could mean Apple has a greater chance of surprising on revenue, both to the upside as well as the downside. Despite Apple’s progress in growing its Services business, as well its other non-iPhone businesses, iPhone still accounted for 48% of June 2019 quarterly revenue.

Those weren’t the only two companies to feel the pinch of the Apple event. Another was Netflix (NFLX) as Apple joined Select List resident Walt Disney (DIS) in undercutting Netflix’s monthly subscription rate. In case you missed it, Disney’s starter package for its video streaming service came in at $6.99 per month. Apple undercut that with a $4.99 a month price point for its forthcoming AppleTV+ service, plus one year free with a new device purchase. To be fair, out of the gate Apple’s content library will be rather thin in comparison to Disney and Netflix, but it does have the balance sheet to grow its library in the coming quarters.

Apple also announced that its game subscription service, Apple Arcade, will launch on September 19 with a $4.99 per month price point. Others, such as Microsoft (MSFT) and Alphabet (GOOGL) are targeting game subscription services as well, but with Apple’s install base of devices and the adoption of mobile gaming, Apple Arcade could surprise to the upside.

To me, the combination of Apple Arcade and these other game services are another nail in the coffin for GameStop (GME).

GameStop – It’s only going to get worse

I’ve been bearish on GameStop (GME) for some time, but even I didn’t think it could get this ugly, this fast. After the close last night, GameStop reported its latest quarter results that saw EPS miss expectations by $0.10 per share, a miss on revenues, guidance on its outlook below consensus, and a cut to its same-store comps guidance. The company also shared the core tenets of a new strategic plan.

Nearly all of its speaks for itself except for the strategic plan. Those key tenets are:

Optimize the core business by improving efficiency and effectiveness across the organization, including cost restructuring, inventory management optimization, adding and growing high margin product categories, and rationalizing the global store base.

Create the social and cultural hub of gaming across the GameStop platform by testing and improving existing core assets including the store experience, knowledgeable associates and the PowerUp Rewards loyalty program.

Build digital capabilities, including the recent relaunch of GameStop.com.

Transform vendor and partner relationships to unlock additional high-margin revenue streams and optimize the lifetime value of every customer.

Granted, this is a cursory review, but based on what I’ve seen I am utterly unconvinced that GameStop can turn this boat around. The company faces headwinds associated with our Digital Lifestyle investing theme that are only going to grow stronger as gaming services from Apple, Microsoft and Alphabet come to market and offer the ability to game anywhere, anytime. To me, it’s very much like the slow sinking ship that was Barnes & Noble (BKS) that tried several different strategies to bail water out.

Did GameStop have its time in the sun? Sure it did, but so did Blockbuster Video and we all know how that ended. Odds are it will be Game Over for GameStop before too long.

Getting back to Apple, now we wait for September 20 when all the new iPhone models begin shipping. Wall Street get your spreadsheets ready!

Elliot Management gets active in AT&T, but its prefers Verizon?

Earlier this week, we learned that activist investor Elliot Management Corp. took a position in AT&T (T). At $3.2 billion, we can safely say it is a large position. Following that investment, Elliot sent a 24-page letter telling AT&T that it needed to change to bolster its share price. Elliot’s price target for T shares? $60. I’ll come back to that in a bit.

Soon thereafter, many media outlets from The New York Times to The Wall Street Journal ran articles covering that 24-page letter, which at one point suggested AT&T be more like Verizon (VZ) and focus on building out its 5G network and cut costs. While I agree with Elliot that those should be focus points for AT&T, and that AT&T should benefit from its spectrum holdings as well as being the provider of the federally backed FirstNet communications system for emergency responders, I disagree with its criticism of the company’s media play.

Plain and simple, people vote with their feet for quality content. We’ve seen this at the movie box office, TV ratings, and at streaming services like Netflix (NFLX) when it debuted House of Cards or Stranger Things, and Hulu with the Handmaiden’s Tale. I’ve long since argued that AT&T has taken a page out of others’ playbook and sought to surround its mobile business with content, and yes that mobile business is increasingly the platform of choice for consuming streaming video content. By effectively forming a proprietary content moat around its business, the company can shore up its competitive position and expand its business offering rather than having its mobile service compete largely on price. And this isn’t a new strategy – we saw Comcast (CMCSA) do it rather well when it swallowed NBC Universal to take on Walt Disney and others.

Let’s also remember that following the acquisiton of Time Warner, AT&T is poised to follow Walt Disney, Apple and others into the streaming video service market next year. Unlike Apple, AT&T’s Warner Media brings a rich and growing content library but similar to Apple, AT&T has an existing service to which it can bundle its streaming service. AT&T may be arriving later to the party than Apple and Disney, but its effort should not be underestimated, nor should the impact of that business on how investors will come to think about valuing T shares. The recent valuation shift in Disney thanks to Disney+ is a great example and odds are we will see something similar at Apple before too long with Apple Arcade and AppleTV+. These changes will help inform us as to how that AT&T re-think could play out as it comes to straddle the line between being a Digital Infrastructure and Digital Lifestyle company.

Yes Verizon may have a leg up on AT&T when it comes to the current state of its 5G network, but as we heard from specialty contractor Dycom Industries (DY), it is seeing a significant uptick in 5G related construction and its top two customers are AT& T (23% of first half 2019 revenue) followed by Verizon (22%). But when these two companies along with Sprint (S), T-Mobile USA (TMUS) and other players have their 5G network buildout competed, how will Verizon ward off subscriber poachers that are offering compelling monthly rates?

And for what it’s worth, I’m sure Elliot Management is loving the current dividend yield had with T shares. Granted its $60 price target implies a yield more like 3.4%, but I’d be happy to get that yield if it means a 60% pop in T shares.

California approves a bill that changes how contract workers are treated

California has long been a trend setter, but if you’re an investor in Uber (UBER) or Lyft (LYFT) — two companies riding our Disruptive Innovators theme — that latest bout of trend setting could become a problem. Yesterday, California lawmakers have approved Assembly Bill 5, a bill that requires companies like Uber, Lyft and DoorDash to treat contract workers as employees.

This is one of those times that our thematic lens is being tilted a tad to focus on a regulatory change that will entitle gig workers to protections like a minimum wage and unemployment benefits, which will drive costs at the companies higher. It’s being estimated that on-demand companies like Uber and the delivery service DoorDash will see their costs rise 20%-30% when they rely on employees rather than contractors. For Uber and Lyft, that likely means pushing out their respective timetables to profitability.

We’ll have to see if other states follow California’s lead and adopt a similar change. A coalition of labor groups is pushing similar legislation in New York, and bills in Washington State and Oregon could see renewed momentum. The more states that do, the larger the profit revisions to the downside to be had.

Volkswagen set to disrupt the electric vehicle market

It was recently reported that Volkswagen (VWAGY) has hit a new milestone in reducing battery costs for its electric vehicles, as it now pays less than $100 per KWh for its batteries. Given the battery pack is the most expensive part of an electric vehicle, this has been thought to be a tipping point for mass adoption of electric vehicles.

Soon after that report, Volkswagen rolled out the final version of its first affordable long-range electric car, the ID.3, at the 2019 Frankfurt Motor Show and is expected to be available in mid-2020. By affordable, Volkswagen means “under €30,000” (about $33,180, currently) and the ID.3 will come in three variants that offer between roughly 205 and 340 miles of range.

By all accounts, the ID.3 will be a vehicle to watch as it is the first one being built on the company’s new modular all-electric platform that is expected to be the basis for dozens more cars and SUVs in the coming years as Volkswagen Group’s pushed hard into electric vehicles.

Many, including myself, have been waiting for the competitive landscape in the electric vehicle market to heat up considerably – it’s no secret that all the major auto OEMs are targeting the market. Between this fall in battery cost and the price point for Volkswagen’s ID.3, it appears that the change in the landscape is finally approaching and it’s likely to bring more competitive pressures for Clean Living company and Cleaner Living Index constituent Tesla (TSLA).

Plus the Biggest Threat to the German Auto Industry

On this episode of the Thematic Signals podcast, we’re digging into the July Retail Sales and quarterly earnings results from Walmart as both confirm the hard-blowing tailwinds associated with our Digital Lifestyle, Middle-Class Squeeze, Aging of the Population and Cleaner Living Investing themes.

We also breakdown a recent article in The Wall Street Journalthat discusses how one aspect of our Cleaner Living investing theme — electric vehicles — could threaten the German economy. It’s the same structural shift that should have folks more than a little concerned about Tesla, both its business as well as its shares. All that and much more on this episode of the podcast.

Boosting our stop loss on Middle-Class Squeeze Thematic Leader Costco Wholesale (COST) to $240.

Safety & Security Thematic Leader Axon Enterprise Inc. (AAXN) catches a TAZR win.

Housekeeping: The next issue of Tematica Investing will be published during the week of July 29th. Why? Because next week I will be on vacation. Even though I’ll be catching up on some reading and thematic thinking, I’ll be kicking back and recharging for what lies ahead.

Last week, we started the June-quarter earnings season. While there were only 20 reports, what we heard from BASF SE, Fastenal (FAST), and MSC Industrial (MSM) served to remind us that, even though the Fed will likely cut interest rates, odds are the current earning seasons will be a challenging one. That view was reaffirmed this week with results from JB Hunt (JBHT) and CSX (CSX) that confirmed the slowdown in freight traffic, an indicator that we here at Tematica watch rather closely as a gauge for the domestic economy’s health.

Given the declines in the Cass Freight Index over the last seven months, the results out of JB Hunt, CSX and other shippers should hardly be news to the investment community. On the other hand, what is somewhat concerning to me is that these declines in freight are coming in even as June Retail Sales surprise to the upside and e-tailers, like Thematic King Amazon (AMZN), Walmart (WMT), Target (TGT) and others, are embracing one-day and same-day shipping from the prior table stakes that were two-day shipping. The growing concern that I have is that despite the tailwind associated with our Digital Lifestyle investing theme, continued declines in the Cass Freight Index and other freight indicators could signal that the domestic economy is moving from one that is slowing into one that is in contraction territory.

Despite the upside surprise in the June Retail Sales report, it was counterbalanced by a revelation contained in the June Industrial Production & Capacity Utilization report. What we learned yesterday from that report was that domestic factory production fell at an annualized rate of 2.2% in the June quarter. Paired with the slowing freight-related signals mentioned earlier, there is little question over the vector of the domestic economy. Clearly the June quarter will be slower than the March one, but the real question we need to face as investors is, how slow will it be in the current third quarter, as well as the fourth quarter this year? That speed along with the degree of the expected July Fed rate cut and the continuation of the current US-China trade war will influence business spending and earnings expectations for the back half of the year.

As far as the June Retail Sales report goes, while I am all for consumers spending, I’m not in love with the fact that it is increasing credit card debt that is likely driving it. According to data collected by the FDIC and published by MagnifyMoney, “Americans paid banks $113 billion in credit card interest in 2018, up 12% from the $101 billion in interest paid in 2017, and up 49% over the last five years.” And as we’ve seen in the monthly Consumer Credit Report issued by the Federal Reserve, revolving consumer credit, which includes credit card balances, has only grown year to date. In other words, consumers are using credit card debt to fund their spending and rising interest payments will squeeze disposable income levels.

While increasing consumer debt is not exactly an uplifting thought, and certainly a headwind for the economy in the coming quarters, these development are a tailwind for Middle-Class Squeeze Thematic Leader Costco Wholesale (COST):

Year to date, COST shares are up some 37%, and we are only now heading into the seasonally strongest time of the year for the company’s business. We should continue to hold COST shares, but we will also increase our stop loss to $240 from roughly $225.

Thematic Leader dates to watch

With investor attention turning to corporate earnings, here are the announced reporting dates for the Thematic Leaders:

Netflix (NFLX) – July 17

Chipotle Mexican Grill (CMG) – July 23

Amazon (AMZN) – July 25

AMN Healthcare (AMN) – August 6

Dycom Industries (DY) – N/A

Costco Wholesale (COST) – N/A

Alibaba (BABA) – N/A

Axon Enterprises (AAXN) – N/A

Not all of the Leaders have shared the reporting dates for their latest quarterly earnings, but no worries as I’ll be filling the calendar in as the missing ones announce them. And it goes without saying that as the June 2019 earning season continues, I’ll be sifting through the sea of reports looking for thematic data points to be had.

As I was putting this issue of Tematica Investing to bed, I saw that Safety & Security Thematic Leader Axon Enterprises (AAXN) announced a big win for its business — a significant order for its TASER Conducted Energy Weapons from agencies across the United States. These orders, which were landed during the first half of 2019, will ship in multiple phases in the coming quarters.

Why are we only hearing about this now?

Partly because Axon needed permission from the agencies make the announcement, and even with such permission granted, the company still needed further permission to name those agencies as customers. A full list of those announced orders can be found here.

Of course, this news is a positive for Axon, and it serves as a reminder that even though the headline story for Axon is the company’s ongoing transformation into a digital security company as it grows it body-camera and digital subscription storage business, the steadfast TAZR business remains a firearm alternative.

We’ve enjoyed a nice run in Axon shares since they were added to the Thematic Leader board, and year to date the shares are up more than 46%. I see no reason to abandon them just yet and our long-term price target of $90 remains intact. For now, our stop loss on the shares continues to sit at $51.

And for what it’s worth, as impressive as that year to date gain is for AAXN shares, it still trails behind Cleaner Living Leader Chipotle Mexican Grill (CMG), which as of last night’s close was up more than 76% year to date.

The G20 meeting will set the stage for what the Fed does next

Earnings expectations have yet to follow GDP expectations lower

We are implementing a $340 stop loss on Digital Lifestyle Thematic Leader Netflix (NFLX).

Over the last few days several economic data points have reinforced the view that the domestic economy is slowing. Meanwhile, the continued back and forth on the trade front, between the U.S. and China as well as Mexico, has been playing out.

What has really captured investors’ focus, however, is the Federal Reserve and the comments earlier this week from Fed Chair Jerome Powell that the Fed is monitoring the fallout from trade issues and eyeing the speed of the economy. Powell said the Fed will “act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective.”

This has led to a pronounced shift in the market, from bad economic data is bad news for the market, to bad news for the economy and trade is good news for the Fed to take action and cut interest rates.

In other words, after the disappointing one-two punch of the IHS Markit US PMI and May ISM Manufacturing Index data, combined with the sharp uppercut that was the May ADP Employment Report, “hopium” has returned to the market.

Over the weekend, we received signs the potential trade war with Mexico will be averted, though few details were shared. China is up next, per comments from U.S. Treasury Secretary Mnuchin, who warned Beijing of tariffs to come if it does not “move forward with the deal … on the terms we’ve done.”

“If China doesn’t want to move forward, then President Trump is perfectly happy to move forward with tariffs to re-balance the relationship,” Mnuchin said.

Near-term, we’re likely to see more “bad news is good news” for the stock market as evidenced by Friday’s market rally following the dismal May jobs report that fell well short of expectations. More economic bad news is being greeted as a positive right now by the market under the belief it will increase the likelihood of the Fed cutting rates sooner than expected.

While that data has indeed led to negative GDP expectation revisions for the current quarter as well as the upcoming one, this new dynamic moved the market higher last week and helped reverse the sharp fall in the market in May, when the major stock indices fell between 6.5% and 8.0%.

As I see it, while the Fed has recently done a good job of telegraphing its moves, the new risk is the market over-pricing a near-term rate cut.

The next Fed monetary policy meeting is less than two weeks away and already expectations for a rate cut exiting that two-day event have jumped to around 21% from less than 7% just over a month ago, according to the CME FedWatch Tool.

Let’s remember there are four more Fed monetary policy meetings — in July, September, October and December — and those give the Fed ample room to cut rates should the upcoming G20 Osaka Summit on June 28-29 fail to get U.S.-China trade talks back on track.

To me, this makes the next two weeks imperative to watch and to build our shopping list. If there is no trade progress coming out of the G20 meeting, it increases the potential for a July rate cut. If trade talks are back on track, we very well could see the Fed continue its current wait-and-see approach.

And what about that potential for over-pricing a rate cut into the market? Anyone who has seen the Peanuts cartoons knows what happens when Lucy yanks the football out from under Charlie Brown at the last minute as he goes to kick it. If you haven’t, we can assure you it never ends well, and the same is true for the stock market when its expectations aren’t fulfilled.

I talk much more about this on this week’s Thematic Signals podcast, which you can listen to here.

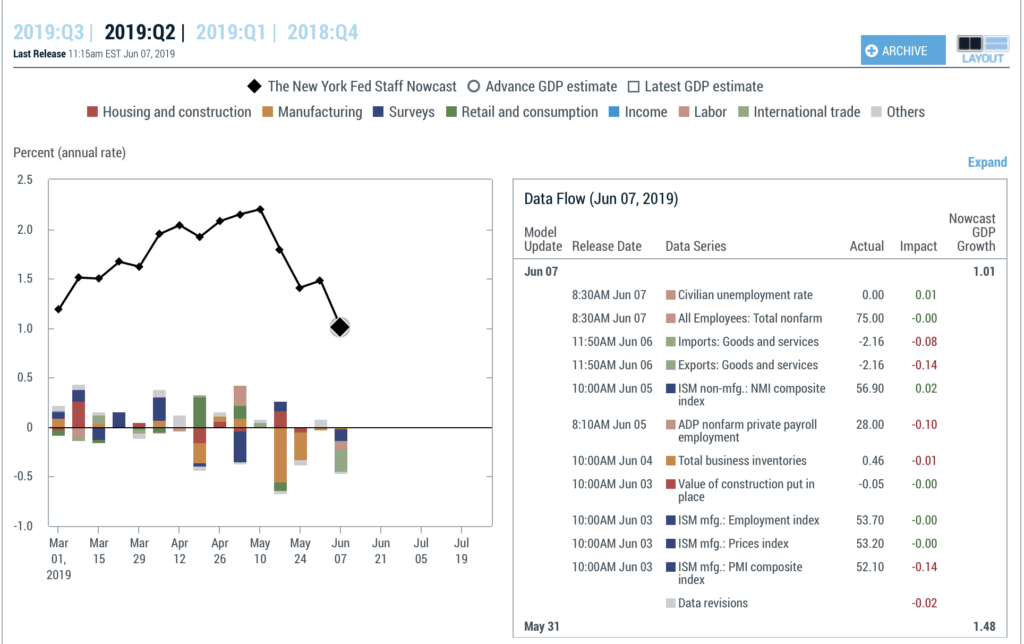

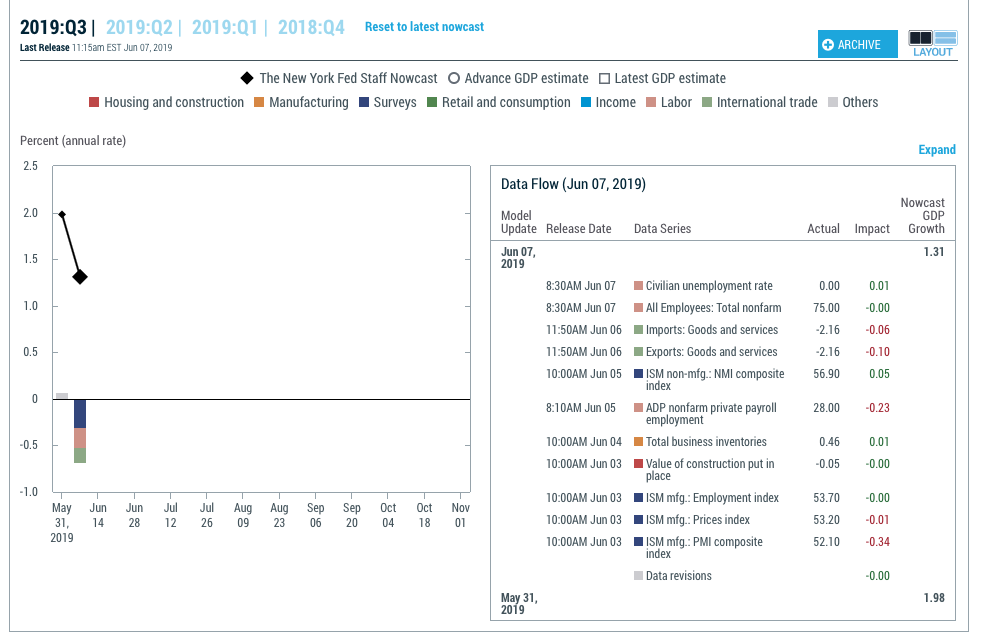

Earnings expectations have yet to follow GDP expectations lower

Here at Tematica our view is that one of the clear-cut risks we face in the current market environment is the over- pricing in of a Fed rate cut at a time when profit and EPS expectations are likely to be revised lower for the second half of 2019. When we see falling GDP expectations like those depicted in the two charts above, it stands to reason we will likely see, at a minimum and barring any substantial trade progress at the G20 summit, companies adopt a more cautious tone for the back half of the year in the coming weeks as we enter the June quarter earnings season.

If that proves to be the case, we are likely to see negative revisions to EPS expectations for the second half of the year. Despite the slowing economic data and impact of tariffs, current expectations still call for an 11% increase in earnings for the S&P 500 in the second half of the year compared to the first half. Viewed a different way, those same expectations for the second half of 2019 call for mid-single digit growth on a year over year basis. To me, given the current backdrop there seems to be more downside risk to those expectations than upside surprise.

Between now and then, we should be listening closely as management teams hit the investor conference circuit this week and next. This week alone brings the Stifel Inaugural Cross Sector Insight Conference 2019, Morgan Stanley U.S. Financials Conference 2019, JP Morgan European Automotive Conference 2019, UBS Asian Consumer, Gaming & Leisure Conference 2019, Deutsche Bank dbAccess 16th Global Consumer Conference 2019, Nasdaq 40th Investor Conference 2019 and the Goldman Sachs 40th Annual Global Healthcare Conference 2019, to name just a few. What we’ll be listening for is updated guidance as well as industry comments, including any tariff impact discussion.

In my view, the conferences and the information spilling out of them will reveal what we are likely to see and hear from various industry leaders in the upcoming June- quarter earnings season.

Tematica Investing

The June rebound in the stock market propped up a number of the Thematic Leaders, most notably Cleaner Living leader Chipotle Mexican Grill (CMG) and Safety & Security leader Axon Enterprises (AAXN). Digital Infrastructure Leader Dycom Industries continues to tread water on a year to date basis, but with 5G deployments accelerating I see a more vibrant landscape for it as well as Disruptive Innovator Leader Nokia (NOK).

In recent weeks, we’ve gotten greater clarity and insight into forthcoming streaming video services from Apple (AAPL) and Disney (DIS), which are likely to make that market far more competitive than it has been to date. Disney’s rumored $6.99 per month starter price recently led Comcast (CMCSA) to not only abandon its own streaming initiative due in 2020 but to also sell its stake in Hulu to Disney. That to me is a potential game changer depending on how Disney folds Hulu’s streaming TV service into Disney+.

One of our key tenants is to observe the shifting landscape, and with regard to streaming video we are seeing the beginning of such a shift. For that reason as well as the risk of a challenging June quarter earnings season in the coming weeks, we are implementing a $340 stop loss on Digital Lifestyle Thematic Leader Netflix (NFLX). That will lock in a profit of just over 27% for NFLX shares.

Later this week, we’ll get the May Retail Sales report, which should once again showcase the accelerating shift to digital shopping. In my view, it’s just another positive data point to be had for Thematic King Amazon (AMZN)… as if all the UPS and other delivery vehicles aren’t enough proof.

Welcome to the Thematic Signals podcast, where we look to distill everyday noise into clear investing signals using our thematic lens and our 10 investing themes. Every week we not only discuss key events that are shaping the stock market, but we also look at key sign posts for the changing economic, demographic, psychographic, and technological landscapes that are driving the structural changes occurring around us.

On this episode, with retailer earnings in the spotlight, we dig into which ones are winning the fight for consumer wallet share and those that are losing. The implications are huge given that retail accounts for nearly 20% of the S&P 500 and roughly 16% of US GDP. Those that are winning the wallet share fight, such as Target, Hibbett Sports, Walmart, TJX Companies. Best Buy and others are leveraging our Middle-Class Squeeze, Digital Society and to a lesser extent our Aging of the Population investing theme. We also talk about what investors should be looking for next as earnings season winds down and share some of the latest signals for our 10 investing themes.

Given the favorable upside to downside risk in AT&T (T) shares, the defensive mobile business and enviable dividend, we are adding T shares to the Select List with a $40 price target as part of our Digital Lifestyle investing theme.

For the stock market, uncertainty remains the name of the game

The stock market looked poised to rebound Friday following President Trump’s prediction of a swift end to the trade war with China. However, the rally faded as investors and traders braced for potential weekend uncertainty on the trade front.

The fade in the stock market capped off a week in which all the major indices closed lower for the fifth consecutive time, pushing their quarter-to-date returns into the red. That has continued in this week as trade tensions escalated further complete with US Secretary of State Mike Pompeo saying the U.S. “may or may not” get a trade deal with China. As we all know, if there is one thing the stock market does not like it’s uncertainty and currently, we have that in spades.

In addition to increasing trade concerns, which included fallout on technology suppliers from the Huawei ban, the latest round of economic data still points to a slowing global economy. Last week, the U.S. economy saw a slump on April core capital goods orders and continued declines in the May IHS Markit Flash U.S. PMI, with soft orders for the month. In response, the New York Fed’s Nowcasting forecast for the current quarter fell to 1.4% on Friday from 1.8% on the prior one, very near the 1.3% forecast by the Atlanta Fed’s GDPNow. We saw similar month-over-month declines in the April IHS Markit Flash Eurozone PMI and Nikkei Flash Japan Manufacturing PMI, which further points to a slowing global economy.

The bottom line: As we exited last week and entered this one, we have an uncertain outlook on the U.S.-China trade front as the global economy continues to slow.

This likely means the market will teeter totter on the latest trade talk comments in the near term. But, as we’ve seen in recent weeks, it will take real progress to convince us and other investors those negotiations are moving forward.

With the earnings season wrapping up, it also means we will soon be entering investor conference season, during which companies will share developments in their respective industries and businesses. Given the factors addressed above, we could very well see them revise their near-term forecasts to the downside. Should that come to pass it more than likely means the recent market declines will be added to.

From my perspective, it means examining and adding companies that sit at the intersection of our 10 investing themes and have defensive business models, preferably with a domestic focused business. It just so happens I have one in mind…

Tematica Investing

Ringing up AT&T shares to the Select List

As trade tensions have heated up and we continue to get more economic data pointing to a slowing domestic economy, we are adding to our position in AT&T given its sticky mobile service that is essentially a digital utility in today’s world, the enviable dividend near 6.3%, and prospects for investors to revisit how they value the shares once the company launches its own streaming platform, WarnerMedia.

Digging into each of these reasons a bit further, in today’s world in which people have an unquenchable thirst for mobile content be it streaming music, video, podcasts; messaging and emailing; shopping or paying bills, smartphones and other connected devices are increasingly “must-haves” in today’s connected world. Plain and simple, AT&T’s mobile business is a Digital Lifestyle access point for consumers.

In my view that not only makes for a sticky business model in today’s connected world, but an inelastic one as well. This means which means there is a high probability those subscribers will pay those bills to keep themselves connected. This makes AT&T and other major mobile network companies rather defensive in today’s environment.

With AT&T, the dividend yield, which is far higher than the 4.0% at Verizon (VZ:NYSE) infers modest downside but also implies upside to be had as the company continues to reassure investors it is right sizing its balance sheet with ample cash flow to remain a company that has been steadily inching up its quarterly dividend for more than 20 years. Recently AT&T sold its 10% stake in Hulu for $1.43 billion to Disney (DIS) and management has commented it has several other “asset monetization alternatives” underway.

The opportunity we see with AT&T shares in the coming months is a valuation transformation similar to the one we recently saw with Select List resident Walt Disney (DIS) that boosted its share price to $130-$135 from $110-$115. Similar to Disney and Disney+, AT&T is slated to launch its own streaming service later this year that will leverage the Time Warner library. Unlike Disney, AT&T exited March with a mobile subscriber base that tallied 79.7 million in size, which offers a target-rich platform for service bundling. As we saw with the final episode for Game of Thrones, which had a reported 19.3 million viewers, people will flock to content they want to watch. Odds are AT&T will offer standalone subscriptions to WarnerMedia rather than an AT&T mobile service bundle only, if only to address how it will AT&T monetize WarnerMedia outside of markets it offers mobile service.

To us that makes AT&T shares a near-term safe harbor stock that is on the cusp of changing how investors value it. That valuation transformation is likely to unlock the share value associated with the synergies to be had with the AT&T-Time Warner merger. And we haven’t even touched on its advertising and analytics business, Xandr, that also stands to benefit from the WarnerMedia launch. More on that as we better understand the relationship to be had between the two business units.

Over the 2011-2018 period, AT&T shares traded in a dividend yield range from a low of 4.9% to a high of 6.1% vs. the current 6.3%. Again, this suggests limited downside from the current share price provided the company continues to make its quarterly dividend payments to shareholders, something the management team has committed to. That historical range established potential peak and trough price levels for AT&Ts’ shares between $34-$42 based on its expected 2019 dividend payment of $2.05 per share.

Given the favorable upside to downside risk in AT&T (T) shares, the defensive mobile business and enviable dividend, we are adding T shares to the Select List with a $40 price target as part of our Digital Lifestyle investing theme.

Coming into this week 15% of the S&P 500 companies have reported and exiting it that percentage will jump to 45%. What the market and investors will be focusing on this week is what led to upside or downside surprises for the reported quarter and how is the current quarter shaping up relative to expectations. Remember, that during the March quarter we saw downward revisions in S&P 500 EPS expectations for the quarter such that the consensus called for EPS declines year over year. Currently, expectations for the current June quarter are up 10% sequentially but are flat year over year.

If we get the data to show these March reports and prospects for the current quarter are better than expected or feared, we could see the 2019 view for S&P 500 earnings move higher vs. the meager 3.7% growth forecast to $167.95. If that happens, it will mark a change in view for 2019 expectations, which have been eroding over the last several months, and could drive the market higher. However, if we see a pickup in downward EPS cuts, we could see those 2019 S&P 500 consensus expectations come under pressure, which would make the stock market even more expensive following its year to date run of 16%.

Now to sift through the onslaught of more than 680 companies reporting this week, which based on what we’re seeing this morning from Coca-Cola (KO), Lockheed Martin (LMT), Twitter (TWTR) and Pulte Group (PHM) suggest potential upside to be had. Tucked inside those results were positive data points for several of our investing themes:

Coca-Cola is feeling the tailwind of our Cleaner Living investing theme as sales of its flavored waters and sports drinks rose 6% year over year, significantly faster than the 1% growth posted by its carbonated drinks business. During the earnings conference call, CEO James Quincy shared that the management team is looking to make Coca-Cola a “total beverage company” by adding coffees, teas, smoothies and flavored waters to a portfolio that has traditionally offered aerated drinks.

Lockheed Martin Corp reported better-than-expected quarterly profit yesterday, benefitting from theSafety & Securitytailwind associated with President Donald Trump’s looser policies on foreign arms sales boosted demand for missiles and fighter jets.

Efforts to improve its advertising business model helped Twitter capture some of our Digital Lifestyletailwind as year over year monetizable daily user growth returned to double digits for the first time in several quarters.

Verizon (VZ) beat quarterly expectations and on its earnings conference call 5G and its deployment in the coming quarters was a key topic during the question and answer session. Verizon will continue to build out its network and bring more 5G capable smartphones to market, which in my view continues to bode well for our Digital InfrastructureandDisruptive InnovatorsThematic Leaders, Dycom (DY) and Nokia (NOK). Nokia will report its quarterly results later this week, and following Ericsson’s better than expected results that tied to strength in North America and 5G, Nokia could surprise on the upside as well.

Splitting the Housing and Retail Sales hairs

Late last week we received some conflicting economic data in the form of the March Retail Sales report and the March Housing Starts data. While retail sales for the month came in stronger than expected — a welcome sign following the last few months in which that data disappointed relative to expectations — March housing starts fell to their weakest point since 2017 despite a tick down in mortgage rates. Now let’s take a deeper dive into those two reports:

In looking at the March Retail Sales report, total retail rose 1.7% month over month (3.5% year over year) with broad-based sales strength and nice gains seen across discretionary spending categories. While we are quite pleased with the month’s data, subscribers know we tend to favor a longer-term perspective when it comes to identifying data trends. Consequently, as we are bracing for the March quarter earnings onslaught it makes sense to examine how retail sales in this year’s March quarter compared to the year-ago quarter. Here we go:

Leaders for the March 2019 quarter vs. March 2018 quarter:

Nonstore retailers up more than 11%, which bodes very well for Thematic King Amazon (AMZN) and to a lesser extent our Alphabet (GOOGL). Let’s remember that those packages need to get to their intended destinations, which likely means positive things for United Parcel Service (UPS), and I’ll be checking that report, which is out later this week.

Food services & drinking places rose 4.4%, which points to favorable data for Guilty Pleasure Thematic Leader Del Frisco’s Restaurant Group (DFRG). And yes, I continue to wait on more about its strategic review process.

Health & personal care stores were up 4.6%.

Building material & garden suppliers and dealers increased by 4.7%.

Laggards for the March 2019 quarter vs. March 2018 quarter:

Sporting goods, hobby, musical instrument, & book stores were down 7.9

Department Stores fell 3.8%, which comes as no surprise to me given the accelerating shift to digital shopping that is part of our Digital Lifestyle investing theme.

Miscellaneous store retailers were down 3.8%

Turning to the March Housing Starts report, the aggregate starts data fell to the weakest level since 2017, but that decline includes both single-family and multifamily housing starts. Breaking down those two components, single-family starts were down 0.4% to 781,000, the slowest pace since September 2016, while permits decreased 1.1% to 808,000, the lowest since August 2017. Multifamily starts, which include apartments and condominiums, were unchanged month over month at 354,000, while those permits fell 2.7%.

The March results may have been influenced to some degree by harsh weather in the Northeast, which contended with heavy snowfalls, and in the South as it dealt with record flooding along the Mississippi and Missouri rivers. Even so, the housing data were off despite a decline in the 30-year mortgage rate to roughly 4.15% this month from 4.86% last October, according to data from Marcrotrends. This decline likely signals that consumers are being priced out of the market as developers and home builders continue to struggle with building affordable properties amid rising labor and materials costs. We also must consider the state of the consumer, who is dealing with the impact of higher debt levels across credit cards, auto loans and student loans — a combination that is sapping disposable income and the ability to service mortgages on homes they may not be able to afford.

Generally speaking, most existing homeowners in the U.S. use the capital from selling their current homes to help fund the purchase of their next dwellings. This means we as investors should watch Existing Home Sales data as a precursor to new home sales and housing starts. Despite February’s better-than-expected sequential print, Existing Home Sales have been falling on a year-over-year basis since February 2018.

Per March Existing Home Sales report, which showed a 5.4% sequential drop vs. February and a similar decline vs. a year ago. For the March quarter, existing home sales fell 5.3%, which in our opinion does not augur well for a near-term pick up in the overall housing market, especially as the recent decline in mortgage rates has not jump started new mortgage applications.

Generally speaking, the housing market has two seasonally strong periods during the year, the spring and fall selling seasons, of which spring tends to be the stronger one. This year, it could be argued that harsh weather in various parts of the U.S. has resulted in the spring selling season getting off to a slow start. Leading up to it, we have seen a climb in the inventory of new homes listed for sale, according to Realtor.com. That’s the supply side of the equation, but the side we remain concerned about is demand.

As we get more data in the coming weeks, we’ll be better able to suss out if we are dealing with a weather related situation, a consumer affordability one or some combination of the two. If the data points to a consumer affordability one, we may consider Home Depot (HD), which is a company that cuts across our Middle Class Squeeze and Affordable Luxury investing themes. Through last night, however, HD shares are up some 28% year to date, and are sitting in over bought territory. Should we see a sizable pullback over the coming weeks as more earnings reports are had and digested, this could be one to revisit.

What the March NFIB Small Business Optimism Index had to say

Making sense of the IMF’s latest economic forecast cut

Ahead of Disney’s (DIS) Investor Day today, we continue to have a Buy on Disney (DIS) shares, and our $125 price target is under review

Based on its recent string of monthly same-store-sales reports and year over year progress in warehouse openings, with more to come, I am bumping our price target on Middle-Class Squeeze Leader Costco Wholesale (COST) to $260 from $250.

Our price target on Thematic King Amazon (AMZN) shares remains $2,250.

Our price target on Alphabet/Google (GOOGL) shares remains $1,300.

What the March NFIB Small Business Optimism Index had to say

This past Tuesday, we received the March Small Business Optimism Index reading from the National Federation of Independent Business (NFIB). The index edged higher, month over month, to 101.8. For the March quarter, the Optimism Index reading averaged 101.56, with March’s reading the highest, which was well below the March 2018 quarter’s 106.4 reading and the 105.5 level for the December 2018 quarter. Clearly, the year-ago level benefited from tax-reform euphoria and while the index has fallen in recent months, the uptrend during first quarter is another sign the domestic economy continues to grow, rather than contract like we are seeing in the Big 3 economies of Europe: Germany, France and Italy.

Digging into the report, one of the bigger soft spots was inventories, as levels were viewed as too large and plans to invest pointed to more firms reducing rather than adding to their inventories. That’s another sign to us of potentially softer guidance relative to expectations in the upcoming earnings season.

Adding to that we also found the Outlook for General Business Conditions component, which looks at the coming six months, has softened considerably, hitting 11 in March, continuing the downtrend in the data since peaking at 35 last July. To us, this reflects that the ongoing trade war, domestic economic data and growing worries over the consumer have taken their toll.

What’s most worrisome to us, however, is the accelerating decline in small business earnings over the last two months. Survey respondents chalk this up to falling sales volume and rising costs that include labor, materials, finance, taxes and regulatory costs.

With lower tax rates and the cut in federal regulation by the Trump administration, the other three factors are the likely culprits behind the month-over-month declines in earnings the last few months. On top of that, the sales expectation for the coming three months has also softened compared to the second half of 2018.

With small business being one of the key job creation engines, these softening sales and earnings expectations could pressure hiring plans and corporate spending, adding to the headwind(s) for the domestic economy.

What’s also interesting ahead of bank earnings that kick off later this week, is the survey revelation that loan availability became harder to obtain during February and March. There was also a drop in expectations for credit in March.

Rather than relying on just one set of numbers, we here at Tematica prefer to leverage several pieces of data to get a fuller, more robust picture. In this case, however, it does mean that we’ll be on guard with bank earnings, especially from those that are outside of the bulge bracket banks — JPMorgan Chase (JPM), Citigroup (C), Bank of America (BAC) and the like. Those names tend to be far more diversified in their revenue streams and can weather the potential storm far better than smaller, regional banks, such as First Community Bankshares (FCBC), that make their profits primarily on deposit and loan volumes.

Making sense of the IMF’s latest economic forecast cut

Also, on Tuesday, the IMF lowered its 2019 World Growth Outlook to 3.3% from 3.5% in January to reflect cuts in both US and European forecasts and a modest upward revision in China. The downward revisions come as the IMF appears to be factoring the recent global economic data that we’ve been getting in recent weeks and in its view “this weakness” is expected to continue in the first half of 2019. Following on that, yesterday morning the European Central Bank (ECB), held interest rates steady and warned that recent data pointed to a “slower growth momentum” in the eurozone.

In many respects these comments were not surprising given the domestic economic and global IHS Markit data we’ve been reviewing here over the last few months. If anything, we see the IMF’s downgrade as overdue. But similar to how the Fed is a cheerleader for the domestic economy, the IMF is forecasting a global economic rebound in 2020, but then proceeds to list a series of downside risks and uncertainties, including “a rebound in Argentina and Turkey and some improvement in a set of other stressed emerging market and developing economies” and a “realization of these downside risks could dramatically worsen the outlook.”

Rather than get wrapped up in the economic forecasts of the IMF, the Fed or other entity, we’ll continue to parse the data and triangulate the data points to get as real-time a view on the domestic and global economy as possible. This includes not only the government issued economic indicators, but also those from trade associations and other third parties. Yesterday we talked on the March Small Business Optimism Index from the NFIB and what it had to say. Other indicators we’ll be watching include monthly truck tonnage data, which fell year over year in February per the American Trucking Association, and weekly rail carloads fell 8.9% year over year in March per data from the Association of American Railroads.

Late yesterday, we received the Fed’s minutes from its March FOMC monetary policy meeting. Recall that exiting the March meeting, the Fed’s post-meeting statement said it would be patient when it comes to future monetary policy actions as it downgraded its GDP forecast in 2019 and 2020. Moreover, it’s updated Economic Projections forecasted only one rate hike between March 2019 and the end of 2020. The meeting minutes confirmed this patient view was widespread across the committee. No surprise there in my view. With inflation data, as well as the vector and velocity of other recent domestic data, tipping lower, I expect the Fed is likely to remain optimistic but dovish in its forthcoming commentary and speeches, especially as the US-China trade negotiations drag on.

And here we go…. March quarter earnings season

The March quarter earnings season “fun” will start off with a trickle of earnings this week, 28 in all including several high-profile bank earnings later this week. The pace will pick up next week when roughly 170 companies will be issuing their results. The following week, which begins on April 22nd, it jumps considerably with more than 700 companies issuing their quarterly results and guidance. It is going to be fast; it is going to be furious.

As you know, over the last few weeks I’ve been increasingly vocal about the potential for a rocky stock market during this earnings season as expectations are likely to get reset for a variety of reasons including the slowing speed of the global economy, dollar headwinds, rising costs, and trade uncertainties to name a few. And let’s remember the March 2018 earnings season saw companies wrap their heads around the impact of tax reform on their collective bottom lines. That bottom-line life preserver, from a guidance perspective, has come and gone. Be sure to hold some downside protection over the next few weeks, like the ProShares Short S&P 500 ETF (SH) shares.

Tematica Investing

First Apple and today Disney

A few weeks ago, Apple (AAPL) held its special event that focused on its Services businesses, specifically the forthcoming streaming video, gaming and news services, all of which look to drive recurring subscription revenue. Today, The Walt Disney Company (DIS) will hold its annual investor meeting at which it will debut Disney+, its own streaming service. The new service from Disney will not only utilize the entire Disney and Fox entertainment library but also build on the company’s direct to consumer efforts with original programming across its Marvel, Star Wars, Pixar and other tentpole franchises.

While DIS shares have not graduated to the Thematic Leaders, they have been on the Select List since mid-2016 as part of our former Content is King investment theme, which has since been folded into the Digital Lifestyle theme. When we first learned of the Disney+ service, my view was that if success is measured by consumer adoption, it had the possibility of transforming how investors should value the company. As more details have emerged on the service, it seems that more across Wall Street have adopted that same view. Earlier this week DIS shares received an upgrade from Cowen & Company to Buy, while BMO Capital Markets raised its rating to Outperform. These moves follow a boost from Goldman Sachs and Rosenblatt Securities last week.

As we move from leaks and rumors on Disney+ to firm details with today’s event — and event that should also touch on other developments as well such as the roll out of Star Wars across Disney’s theme parks — I will revisit my longstanding $125 price target on the shares.

Ahead of Disney’s (DIS) Investor Day today, we continue to have a Buy on Disney (DIS) shares, and our $125 price target is under review

Costco Wholesale does it again in March

Last night Middle Class Squeeze Thematic Leader Costco Wholesale (COST) reported March same-store comps of +5.7% (5.9% excluding gas and foreign exchange.) Compared to the data in recent Retail Sales reports, Costco continues to take consumer wallet share, but to me what was far more striking was the step up in its same-store comps month over month from +3.5% (+4.6% excluding gas and foreign exchange). It would seem it’s not just me looking to fight the tide of rising food prices by buying in bulk at Costco.

The other item that I track rather closely when Costco issues these monthly reports is the number of open warehouses. Exiting March, it had 770 open warehouses, which compares to 749 exiting March 2018. That year over year increase bodes extremely well for Costco as more warehouses delivers increased high-margin membership fee revenue, which generates roughly 70% of the company’s operating income.

Based on its recent string of monthly same-store-sales reports and year over year progress in warehouse openings, with more to come, I am bumping our price target on Middle-Class Squeeze Leader Costco Wholesale (COST) to $260 from $250.

eMarketer sees continued Digital Advertising growth ahead

Ad spending will continue to rise across the globe, with digital driving most of the growth. According to data published by eMarketer, this year worldwide digital ad spending will rise by 17.6% to $333.25 billion, which means that, for the first time, digital will account for roughly half of the global ad market. In my view, this reflects the changing nature of where, how and when we consume content be it video, music, news or some other format that is a key part of our Digital Lifestyleinvesting theme. Advertisers want to go where the eyeballs are, and while this is a tailwind for a number of companies, the change in ad spend location is a growing headwind for “legacy” media companies. No wonder CBS (CBS), Comcast’s (CMCSA) NBC and others are looking to join the streaming video fray.

eMarketer’s forecast depicts one of the core thesis items behind our holding shares of Alphabet Inc. (GOOGL) — namely, that digital advertising will continue to take share of total media spending. Per eMarketer’s forecast, digital advertising will grow to more than 60% of media spending by 2023, up from roughly 46% of advertising last year. While those outer years in the forecast range may be off by a point or two, it’s the direction and year-over-year share gains by digital advertising that matter for our Google shares as well as our Amazon.com (AMZN) shares.

Digging into eMarketer’s forecast, it sees Google remaining the top digital ad seller dog in 2019 with 31% market share. Behind it will be Facebook (FB) and its various properties and then Alibaba (BABA). In fourth place is Amazon, which eMarketer sees as generating $14 billion in ad revenue this year. To most companies, $14 billion would be the business, but at Amazon it should account for roughly 5% of its 2019 revenue. And while it is on the smaller side for the company, it’s bound to be rather profitable.

We are seeing some shifting of ad spend among Google, Facebook and Amazon, with Amazon being the up and comer. That said, the digital ad spend tide is still rising, and with concerns over privacy for Facebook and others the odds are better than good that both Google and Amazon will continue to ride that tide over the next few years. Longer term, as the shift to digital advertising continues, we will see slower growth rates much like any maturing industry, but we’re far from that point today.

Our price target on Thematic King Amazon (AMZN) shares remains $2,250.

Our price target on Alphabet/Google (GOOGL) shares remains $1,300.

This website uses cookies to provide the best experience and to analyze the traffic on our site. Your use of the site serves as your consent for the use of cookies on this site AcceptPrivacy Policy